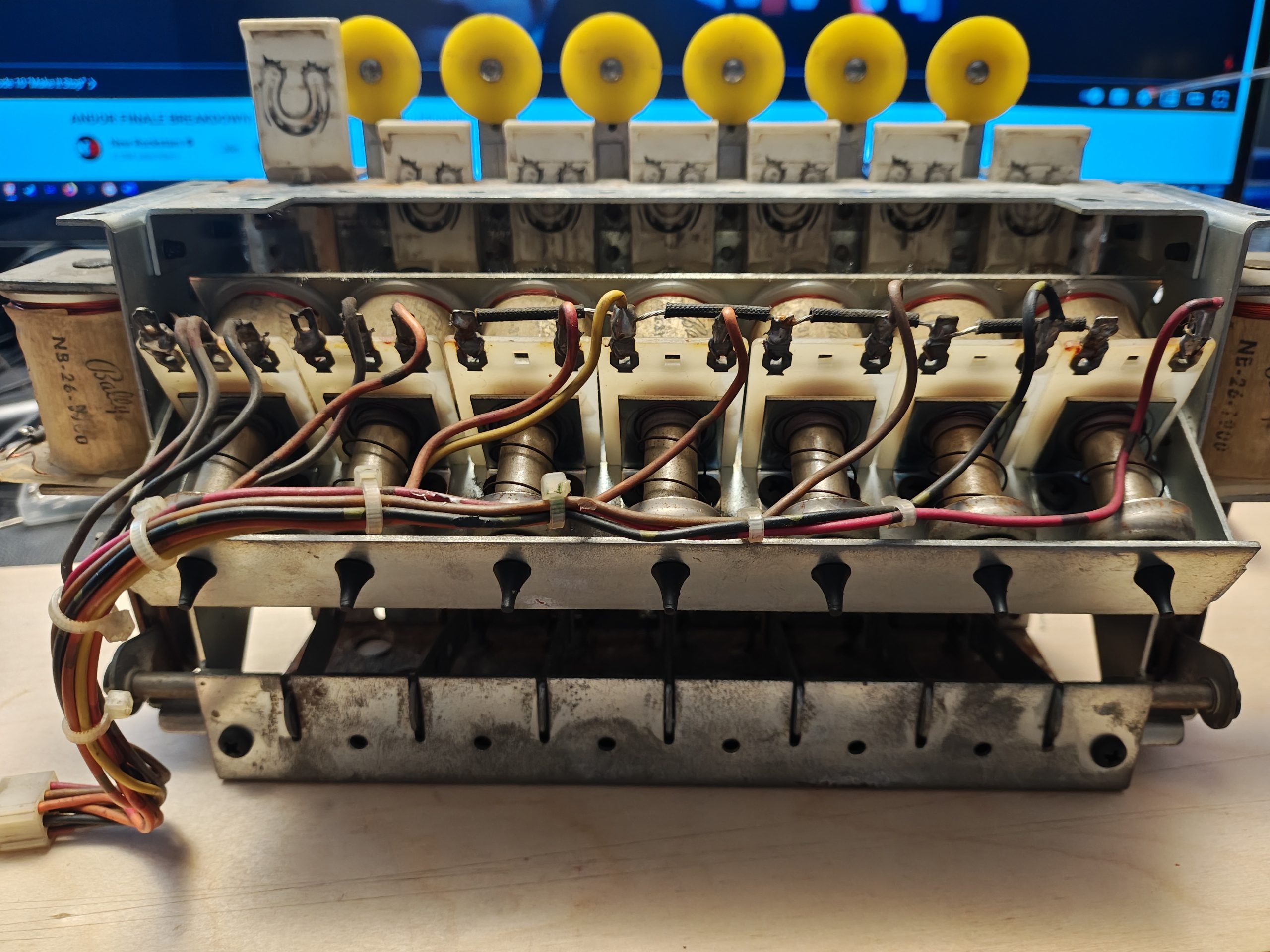

OK, I Finally Took It Apart

I have put off dealing with the large drop target assembly, but finally it was time. It is now cleaned up and in pieces. I hope it goes back together.

Dispatches from District 48

Posts tagged ‘GE’

I have put off dealing with the large drop target assembly, but finally it was time. It is now cleaned up and in pieces. I hope it goes back together.

Nobody really liked Jeff Skilling of Enron and he sits in jail for 20 years. We think Elizabeth Holmes is attractive and cool so that despite the fact that she committed serial fraud in lying about her company's technology and financials (far more baldly and egregiously than Skilling) and actually put people at risk through faulty medical testing, she got only a slap on the wrist.

And then there is Elon Musk.

The Economist used to be boring, but smart with a wicked dry wit. Now it’s just boring (sigh). Tesla will be profitable & cash flow+ in Q3 & Q4, so obv no need to raise money.

— Elon Musk (@elonmusk) April 13, 2018

I am not sure how I got in the role of fact-checking Elon Musk, but given the company's stated results to date and announced operating plans and strategies, there is simply no way for the Tesla to be profitable and cash flow positive in Q3, barring some deus ex machina like a massive energy credit or California subsidy windfall. It's possible I could go in there and shut down R&D and model 3 production and milk the Model S and X for cash and might make this be true, but that is certainly not their announced business plan. On their current path Tesla has to continue to burn cash through the rest of this year. I am not even sure that if you stated their gross margin the same way that other automakers state their numbers that even it would be positive right now -- there is an argument to be made they are still losing money at the margin on every car they produce**. I would add that in this point of their ramp, if you want to see Tesla the huge success that is baked into its current stock valuation, you don't want Tesla to be cash flow positive in the third quarter, you want it continuing to invest. Amazon rules the world because it deferred profitability for years in favor of growth.

Tesla pretty much never ever lives up to Musk's promises, at least for the dates he promises them. That is probably OK with things like deliveries of new products -- people understand he is pushing technology and new products can be delayed and they forgive entrepreneurs for being -- shall we say -- overly enthusiastic about such things. But on financial stuff like this his statements are bordering on fraud. But he'll never get called on it, because we like him in a way we didn't like Skilling.

I will add that if Musk wants to get snippy about the media's guesses about his company's prospects, and thinks we are all getting it wrong, he could sure be a lot more transparent about Tesla's financials and plans. Go watch an Exxon-Mobil analyst presentation and compare it to Musk's quarterly arm-waving. Also, one final memo to Musk: responding to your critics on Twitter emulating Trump's style is not recommended. Though it might be interesting to compare the irrational populist wave behind Trump with the populist wave behind Tesla. Though the two Venn diagrams of supporters probably do not overlap much, the whole relationship feels similar to me.

Disclosure: I have been short TSLA in the past but right now have no position. To be honest, I am going to let Musk urge his fanboys to pump the stock a bit further before I short again. The fanboy effect makes TSLA a dangerous short, as TSLA stock holders will defy reality for far longer than will holders of say GE or XOM.

** gross margin at TSLA is interesting because TSLA has no dealer network, something I like them for. GM discounts its cars to their dealers (10% or so?) but in turn they offload a bunch of selling and support costs to the dealers. In their gross margin, TSLA banks in their gross margin the extra 10% from not having to discount their cars but in turn does not charge gross margin for a lot of the extra sales and support costs they have to take on -- instead they drop these costs into SG&A overhead. The situation with gross margin is even more complicated because Tesla not only has to build out and operate its own warranty service, sales, and delivery network to replace traditional dealers, it is also building out its own fueling service to replace gas stations. Here is one guy who thinks Tesla gross margin is really negative. I have zero idea who he is but for the last year his predictions about Tesla have been a lot more reliable than Musk's statements.

Tesla agreed to give Elon Musk what is potentially the richest executive compensation package ever. I will give my (*gasp*) cynical reason why I think they did this. I can show you in one chart (Tesla Model 3 production, from Bloomberg):

I would argue that Elon Musk is the only one in the world who can run a company with so many spectacular failures to meet commitments and still have investors and customers coming back and begging for more. A relatively large percentage of Teslas get delivered with manufacturing defects and their customers sing their praises (even while circulating delivery defect checklists). Tesla keeps publishing Model 3 production hockey sticks (apparently with a straight face) and consistently miss (each quarter pushing back the forecast one quarter) and investors line up to buy more stock. Tesla runs one of the least transparent major public companies in this country (so much so that people like Bloomberg have to spend enormous efforts just to estimate what is going on there) and no one is fazed. Competitors like Volvo and Volkswagon and Toyota and even GM have started to push their EV technology past Tesla and actually sell more EV's than does Tesla (with the gap widening) and investors still treat Tesla like it has a 10-year unassailable lead on competition.

All because Elon Musk can stand up at a venue like SXSW, wave his hands, spin big visions, and the stock goes up $3 billion the next day. Exxon-Mobil has a long history of meeting promises, reveals its capital spending plans in great detail, but misses on earnings by a few cents and loses $40 billion in market cap. GE lost over half its market value when investors got uncomfortable with their lack of transparency and their failures to meet commitments. Not so at Tesla, in large part because Elon Musk is PT Barnum reincarnated, or given the SpaceX business, he is Delos D. Harriman made real.

Disclosure: I don't currently have any position in TSLA but over the last 2 years I have sold short when it reaches around $350 (e.g. after Elon Musk speaks) and buy to cover around $305 (e.g. when actual operational or financial data is released). Sort of the mirror image of BTFD.

General Electric (GE) has complained for years about Connecticut's (its current corporate home) taxation and regulatory policies. Recently, it said it was moving for greener pastures, and was leaving for... Massachusetts?

Seriously? This is like moving from North Korea to China to get more freedom of speech. Boston's top state income tax bracket is perhaps a point lower than CT's but Florida or Texas have rates of zero, and a much lower cost of living and real estate.

Granted that Boston has its attractions for a company trying to change its public perception to being a technology company. But I can't shake the suspicion this has something to do with a relocation giveaway to GE from the city and state. GE has become one of the biggest supporters and beneficiaries of crony capitalism in the country. I have to believe they cut some sweetheart deal that will eventually funnel a bunch of Massachusetts taxpayer money into GE coffers. After all, if cities will throw away a half billion dollars in taxpayer money to attract an NFL team that does business for just 24 hours a year in the city (8 games x 3 hours per game), how much will politicians pay of their citizens' money to be able to list "attracting GE" as a lead bullet in their re-election talking points?

My headline is probably the most accurate description of how China's devaluation of the yuan yesterday affects this country. But I bet you will not see it portrayed that way in any other media. What you are going to see, particularly as the Presidential election races heat up, are multiple calls to bash China in some way to punish it for being so generous to American consumers. Why? Because the devaluation of the yuan will negatively affect the bottom line of a few export sensitive companies. And if we have learned anything from the Ex-Im battle, things that GE and Boeing like or hate are much more likely to affect policy than things that benefit 300 million consumers. Make no mistake, protectionist measures are the worst sort of cronyism, benefiting a few companies and workers and hurting everyone else (look up concentrated benefits, dispersed costs).

By the way, aren't the worldwide competitive devaluation sweepstakes amazing? If everyone is doing it, then devaluations have no substantive effect on trade (except to perhaps decrease its magnitude in total), which just adds to the utter pointlessness of the game. And it is hilarious to me to see US elected officials criticizing China for "manipulating" its currency, as if the US Fed hasn't added several trillion dollars to its balance sheet over the last few years in a heroic attempt to manipulate the value (downwards) of our own currency.

I am going to oversimplify, but the essence of bank risk is that they borrow short-term and invest/lend long-term. This is a money-making strategy in that one can often borrow short-term much cheaper than one can borrow long term. This spread between long and short term rates is due to people valuing liquidity. You probably have experienced it yourself when buying a certificate of deposit (CD). The rates for 5 or 10 year CD's are higher, but do you really want to tie your money up for so long? What if rates improve and you find yourself locked into a CD with lower rates? What if you need the money for an emergency? Your concern for having your money locked up is what a preference for liquidity means.

So banks live off this spread. But there are risks, just like you understood there are risks to locking your money in a long-term CD. Imagine the bank is lending for mortgages and AAA corporate customers at 6%. To fund that, they have some shareholder money, which is a long-term investment. But they make the rest up with things like deposits and commercial paper (essentially 90-day or shorter notes). We will leave the Fed out for this. There are two main risks

These risks are made worse when banks or bank-like institutions try to improve the spread they are earning by making riskier investments, thus increasing the spread between their borrowing and investing, but also increasing risk. This is particularly so because these risky investments tend to go south at the same time that short-term credit markets dry up. In fact, the two are closely related.

This is exactly what happened to GE. Via MarketWatch:

GE’s news release announcing its latest and greatest reduction of GE Capital summed up the move beautifully, saying “the business model for large wholesale-funded financial companies has changed, making it increasingly difficult to generate acceptable returns going forward.â€

“Wholesale-funded†refers to GE Capital’s traditional reliance on the commercial paper market for liquidity. The problem with this short-term funding model for a balance sheet with long-term assets is that during a financial crisis, overnight liquidity tends to dry up as it did for GE late in 2008. When the company had difficulty finding buyers for its paper, the Federal Deposit Insurance Corp. stepped in and through its Temporary Liquidity Guarantee Program (TLGP) was covering $21.8 billion of GE commercial paper. GE Capital registered for up to $126 billion in commercial-paper guarantees under the TLGP.

If you have a AAA credit rating, you can always, always make money in the good times borrowing short and investing long. You can make even more money borrowing short and investing long and risky. GE made their money in the good times, and then when the model absolutely inevitably fell on its face in the bad times, we taxpayers bailed them out.

Which leads me to think back to Enron. Enron is associated in most people's minds with fraud, and Enron played a lot of funky accounting games to disguise its true financial position from its owners. But at the end of the day, that fraud was not why it failed. Enron failed because it was essentially a bank that was borrowing short and investing long. When the liquidity crisis arrived and they couldn't borrow short any more, they went bankrupt. Jeff Skilling didn't actually go to jail for accounting fraud, he went to jail for making potentially inaccurate positive statements to shareholders to try to head off the crisis of confidence (and the resulting liquidity crisis). Something every CEO in history has done in a liquidity crisis (back in 2008 I wrote an article comparing Bear Stearns crash and the actions of its CEO to Enron's; two days later the Economist went into great depth on the same topic).

So the difference between GE and Enron? The government bailed out GE by guaranteeing its commercial paper (thus solving its problem of access to short term funding) and did nothing for Enron. Obviously the time and place and government officials involved differed, but I would also offer up two differences:

Artist's rendering of 2008 business strategy of GE Capital, Citicorp, Bank of America, Goldman Sachs, GMAC, etc.

Postscript: For those not clicking through, I though this bit from the 2008 Economist article was pretty thought-provoking:

For many people, the mere fact of Enron's collapse is evidence that Mr Skilling and his old mentor and boss, Ken Lay, who died between hisconviction and sentencing, presided over a fraudulent house of cards. Yet Mr Skilling has always argued that Enron's collapse largely resulted from a loss of trust in the firm by its financial-market counterparties, who engaged in the equivalent of a bank run. Certainly, the amounts of money involved in the specific frauds identified at Enron were small compared to the amount of shareholder value that was ultimately destroyed when it plunged into bankruptcy.

Yet recent events in the financial markets add some weight to Mr Skilling's story"â€though nobody is (yet) alleging the sort of fraudulentbehaviour on Wall Street that apparently took place at Enron. The hastily arranged purchase of Bear Stearns by JP Morgan Chase is the result of exactly such a bank run on the bank, as Bear's counterparties lost faith in it. This has seen the destruction of most of its roughly $20-billion market capitalisation since January 2007. By comparison, $65 billion was wiped out at Enron, and $190 billion at Citigroup since May 2007, as the credit crunch turned into a crisis in capitalism.

Mr Skilling's defence team unearthed another apparent inconsistency in Mr Fastow's testimony that resonates with today's events. As Enronentered its death spiral, Mr Lay held a meeting to reassure employees that the firm was still in good shape, and that its "liquidity was strong". The composite suggested that Mr Fastow "felt [Mr Lay's comment] was an overstatement" stemming from Mr Lay's need to "increase public confidence" in the firm.

The original FBI notes say that Mr Fastow thought the comment "fair". The jury found Mr Lay guilty of fraud at least partly because it believed the government's allegations that Mr Lay knew such bullish statements were false when he made them.

As recently as March 12th, Alan Schwartz, the chief executive of Bear Stearns, issued a statement responding to rumours that it was introuble, saying that "we don't see any pressure on our liquidity, let alone a liquidity crisis." Two days later, only an emergency credit line arranged by the Federal Reserve was keeping the investment bank alive. (Meanwhile, as its share price tumbled on rumours of trouble onMarch 17th, Lehman Brothers issued a statement confirming that its "liquidity is very strong.")

Although it can do nothing for Mr Lay, the fate of Bear Stearns illustrates how fast quickly a firm's prospects can go from promising to non-existent when counterparties lose confidence in it. The rapid loss of market value so soon after a bullish comment from a chief executive may, judging by one reading of Enron's experience, get prosecutorial juices going, should the financial crisis get so bad that the public demands locking up some prominent Wall Streeters.

Our securities laws are written to protect shareholders and rightly take a dim view of CEO's make false statements about the condition of a company. But if you owned stock in a company facing such a crisis, what would you want your CEO saying? "Everything is fine, nothing to see here" or "We're toast, call Blackstone to pick up the carcass"?

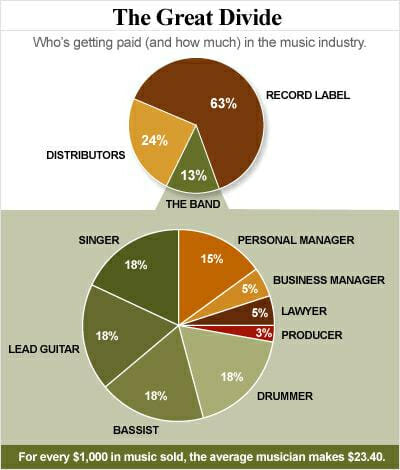

We have all heard that artists make very little money from their songs, and get "ripped off"by record labels and other folks in the chain. I have always had mixed reactions to this. I have no doubt that, with zero power and a burning desire to "make it big", young acts sign uneven deals with record labels. However, I find it hard to believe that Beyonce is getting hosed in that negotiation.

I saw this chart in TechDirt about where the money consumers spend on music goes (I think this is for a CD sale):

So the performers themselves get about 9% of the retail price after everyone in the chain is paid. That certainly seems paltry -- after all, they are the owners and creators of the music. Everyone else is just in the service chain to make sure the music reaches the customers, all the accounting is done, the legal documents are correct, etc.

But it turns out that they may not be doing that badly. I am a shareholder of ExxonMobil (XOM). I own a piece of all the oil that XOM owns and controls, along with all the other shareholders. Think of us as the band, though a really big band with lots of players. That oil we own, like the band's music, has a ton of value. When sold as raw crude, it goes for $40-$60 a barrel nowadays. When sold in pieces (such as gasoline, or asphalt, or lubrication oil) it can sell for hundreds of dollars a barrel.

But out of those proceeds, we have to pay people to help us. We have to pay managers, and lawyers. We have to pay oilfield services companies and equipment companies and transportation companies. We have to pay retailers. When all those payments are made, before taxes, in 2014 we were left with just under 8% of every dollar we sell. We own all this oil and we are not even getting as much as a musician!

And XOM shareholders do pretty well. Owners of Wal-Mart only get about 3% of every dollar they sell. In my company, I get about 5% of every dollar I sell. And those evil health insurers? Their shareholders get just over 2% of every dollar sold (all based on 2014 full-year financials).

Does that mean that Exxon shareholders are getting "ripped off" by Haliburton and Burlington Northern? Is Wal-Mart getting ripped off by Proctor and Gamble? Is Humana getting ripped off by GE imaging? No?

I will reveal the ugly secret: There is one person who is "ripping off" all of these folks, from Exxon to Rihanna to me. That person is.... the consumer. Yep, there are certainly many examples of people signing bad contracts in all these businesses, but the only entity systematically and consistently ripping all these folks off is us. Because in a capitalist economy, we have the ultimate power. We drive down the street to get the gas that is 10 cents cheaper, we now shop for our books and TVs at Wal-Mart and Amazon rather than at Borders and Best Buy, and we buy 99-cent individual songs on iTunes instead of buying a whole CD of songs we don't want for $14.99.

Well, so much for the implicit gag order Obama has had on the insurance companies. Bet we will find out a lot more interesting details about the exchange rollouts now.

[T]he White House has its own idea to stop the bleeding: Allow insurers to renew existing plans in 2014 (which means they could continue into 2015) while forcing them to send Landrieu-like letters explaining why their plans don’t conform to the Affordable Care Act’s standards.

This doesn’t really ensure anyone can actually keep their plan — which means it also doesn’t affect premiums in the exchanges. But it makes it easier for Democrats to blame insurers for canceling these plans. And it perhaps makes it easier for the White House to stop congressional Democrats from signing onto something like Landrieu or Udall.

The insurance industry is furious. They’ve been working with the White House to get HealthCare.Gov up and running and they’ve been devoting countless man hours to dealing with the problems and they’ve been taking the heat from their customers over canceled plans, and now the Obama administration wants to make them into a scapegoat.

“This doesn’t change anything other than force insurers to be the political flack jackets for the administration,” an insurance industry insider told Evan McMorris-Santoro. “So now, when we don’t offer these policies, the White House can say it’s the insurers doing this and not being flexible.”

This is like telling GE to reintroduce 100 watt lightbulbs on thirty days notice, and then blaming them if they don't do it. Or as I tweeted earlier,

Obama telling insurers they can reinstate plans is like my wife telling me to take the exit we passed two miles ago @instapundit @mfcannon

— Coyoteblog (@Coyoteblog) November 14, 2013

Update: Left rallying around Obama, spreading the word that cancellations are all the insurance companies' fault. I am SO glad I am not affiliated with a political party such that I would feel the need to embarrass myself to support some flailing politician on my team.

The Left has been calling cancelled policies "sub-standard" for months now. For three years Obama's own folks were estimating that over half of individual policies would have to be cancelled due to the law, and in fact they purposely wrote the regulations narrower to invalidate the maximum number of policies. But now cancellations are the insurance companies' fault??

Obama and the Left want a big new infrastructure spending bill, based on twin theories that it would be a) stimulative and b) a bargain, as needed infrastructure could be built more cheaply with construction industry over-capacity.

Since this is exactly the same theory of the stimulus four years ago, it seems a reasonable question to ask: What happened to the damn money we spent last time? We were sold a 3/4 of a trillion dollar stimulus on it being mostly infrastructure. So where is it? Show us pictures, success stories. Show us how the cost of construction of these projects were so much lower than expected because of construction industry over-capacity. Show us the projects selected, to demonstrate how well thought-out the investment prioritization was. If their arguments today have merit, all these things must be demonstrable from the last infrastructure bill. So where is the evidence?

Of course, absolutely no one who wants to sell stimulus 2 (or 3?) wants to go down the path of investigating how well stimulus 1 was spent. Instead, here is the argument presented:

Much of the Republican opposition to infrastructure spending has been rooted in a conviction that all government spending is a boondoggle, taxing hard-working Americans to give benefits to a favored few, and exceeding any reasonable cost estimate in the process. That's always a risk with new spending on infrastructure: that instead of the Hoover Dam and the interstate highway system, you end up with the Bridge to Nowhere and the Big Dig.

In that sense, this is a great test of whether divided democracy can work, and whether Republicans can come to the table to govern. One can easily imagine a deal: Democrats get their new infrastructure spending, and Republicans insist on a structure that requires private sector lenders to be co-investors in any projects, deploying money based on its potential return rather than where the political winds are tilting.

This is bizarre for a number of reasons. First, he implies the problem is that Republicans are not "coming to the table to govern" In essence then, it is up to those who criticize government incremental infrastructure spending (with a lot of good evidence for believing so) as wasteful to come up with a solution. Huh?

Second, he talks about requiring private lenders to be co-investors in the project. This is a Trojan horse. Absurd projects like California High Speed Rail are sold based on the myth that private investors will step in along side the government. When they don't, because the project is stupid, the government claims to be in too deep already and that it must complete it with all public funds.

Third, to the extent that the government can sweeten the deal sufficiently to make private investors happy, the danger of Cronyism looms large. You get the government pouring money into windmills, for example, that benefits private investors with a sliver of equity and large manufacturers like GE, who practically have a hotline to the folks who run programs like this.

Fourth, almost all of these projects are sure to be local in impact - ie a bridge that helps New Orleans or a street paving project that aids Los Angeles. So why are the Feds doing this at all? If the prices are so cheap out there, and the need for these improvements so pressing, then surely it makes more sense to do them locally. After all, the need for them, the cost they impose, and the condition of the local construction market are all more obvious locally than back in DC. Further, the accountability for money spent at the Federal level is terrible. There are probably countless projects I should be pissed off about having my tax money fund, but since I don't see them every day, I don't scream. The most accountability exists for local money spent on local projects.

How the recent "fairness" tax bill became a vehicle for subsidizing connected corporations.

Baucus' Finance Committee passed a bill in August extending 50 expiring deductions and credits for favored industries. At Obama's insistence, the Baucus bill was cut and pasted word for word into the cliff legislation. Set aside for a moment how this contradicts Obama's talk about "fair shares" and the need to diminish the influence of lobbyists, and look at what this raft of tax favors shows us about the Baucus Machine.

Pick any one of the special-interest tax breaks extended by the cliff deal, and you're likely to find a former Baucus aide who lobbied for it on behalf of a large corporation or industry organization.

General Electric may have been the biggest winner from the cliff deal. GE makes more wind turbines than any other U.S. company, and it lobbied hard for extension of the wind production tax credit. But more important for the multinational conglomerate was an arcane-sounding provision that became Section 222 of Baucus' bill and then Section 322 of the cliff bill: "Extension of subpart F exception for active financing income."

In short, this provision allows multinationals to move profits to offshore financial subsidiaries and thus avoid paying U.S. corporate income taxes. This is a windfall for GE: The exception played a central role in GE paying $0 in U.S. corporate income tax in 2011 when it made $5.1 billion in U.S. profits.

Peter Prowitt, formerly Baucus' chief of staff, is now an in-house lobbyist and VP at GE. GE filings show Prowitt on the lobbying teams that won wind-tax credits, electric-vehicle tax credits, and "Extension of Subpart F Deferral for Financial Services."

The examples in the article go on and on. The best way to get rich in America is not to have a great idea or work hard but to hire an ex-staffer from Senator Baucus's office.

Almost exactly seven years ago (amazing how long I have been blogging) I wrote an extended piece about how hard it is to change corporate DNA. I was writing about GM but also used Wal-Mart as an example. Part of this piece read:

A corporation has physical plant (like factories) and workers of various skill levels who have productive potential. These physical and human assets are overlaid with what we generally shortcut as "management" but which includes not just the actual humans currently managing the company but the organization approach, the culture, the management processes, its systems, the traditions, its contracts, its unions, the intellectual property, etc. etc. In fact, by calling all this summed together "management", we falsely create the impression that it can easily be changed out, by firing the overpaid bums and getting new smarter guys. This is not the case - Just ask Ross Perot. You could fire the top 20 guys at GM and replace them all with the consensus all-brilliant team and I still am not sure they could fix it.

All these management factors, from the managers themselves to process to history to culture could better be called the corporate DNA*. And DNA is very hard to change. Walmart may be freaking brilliant at what they do, but demand that they change tomorrow to an upscale retailer marketing fashion products to teenage girls, and I don't think they would ever get there. Its just too much change in the DNA. Yeah, you could hire some ex Merry-go-round** executives, but you still have a culture aimed at big box low prices, a logistics system and infrastructure aimed at doing same, absolutely no history or knowledge of fashion, etc. etc. I would bet you any amount of money I could get to the GAP faster starting from scratch than starting from Walmart. For example, many folks (like me) greatly prefer Target over Walmart because Target is a slightly nicer, more relaxing place to shop. And even this small difference may ultimately confound Walmart. Even this very incremental need to add some aesthetics to their experience may overtax their DNA.

Corporate DNA acts as a value multiplier. The best corporate DNA has a multiplier greater than one, meaning that it increases the value of the people and physical assets in the corporation. When I was at a company called Emerson Electric (an industrial conglomerate, not the consumer electronics guys) they were famous in the business world for having a corporate DNA that added value to certain types of industrial companies through cost reduction and intelligent investment. Emerson's management, though, was always aware of the limits of their DNA, and paid careful attention to where their DNA would have a multiplier effect and where it would not. Every company that has ever grown rapidly has had a DNA that provided a multiplier greater than one... for a while.

But things change. Sometimes that change is slow, like a creeping climate change, or sometimes it is rapid, like the dinosaur-killing comet. DNA that was robust no longer matches what the market needs, or some other entity with better DNA comes along and out-competes you. When this happens, when a corporation becomes senescent, when its DNA is out of date, then its multiplier slips below one. The corporation is killing the value of its assets. Smart people are made stupid by a bad organization and systems and culture. In the case of GM, hordes of brilliant engineers teamed with highly-skilled production workers and modern robotic manufacturing plants are turning out cars no one wants, at prices no one wants to pay.

Changing your DNA is tough. It is sometimes possible, with the right managers and a crisis mentality, to evolve DNA over a period of 20-30 years. One could argue that GE did this, avoiding becoming an old-industry dinosaur. GM has had a 30 year window (dating from the mid-seventies oil price rise and influx of imported cars) to make a change, and it has not been enough. GM's DNA was programmed to make big, ugly (IMO) cars, and that is what it has continued to do. If its leaders were not able or willing to change its DNA over the last 30 years, no one, no matter how brilliant, is going to do it in the next 2-3.

Megan McArdle makes some very similar points as I about Wal-Mart and how hard it is to change corporate DNA. I recommend you read the whole thing.

Politicians certainly live in their own world:

The Environmental Protection Agency has slapped a $6.8 million penalty on oil refiners for not blending cellulosic ethanol into gasoline, jet fuel and other products. These dastardly petroleum mongers are being so intransigent because cellulosic ethanol does not exist. It remains a fantasy fuel. The EPA might as well mandate that Exxon hire Leprechauns.

As a screen shot of EPA’s renewable fuels website confirms, so far this year - just as in 2011 - the supply of cellulosic biofuel in gallons totals zero.

“EPA’s decision is arbitrary and capricious. We fail to understand how EPA can maintain a requirement to purchase a type of fuel that simply doesn’t exist,” stated Charles Drevna, president of American Fuel & Petrochemical Manufacturers (AFPM), the Washington-based trade association that represents the oil refining and petrochemicals industries.

I will remind Republicans thought that ethanol is a bipartisan turd, this particular requirement having been signed into law by President Bush.

The arch-corporate-statist -- and official manufacturing company of the Obama Administration is feeding at the trough again. Apparently a perfectly profitable company cannot buy assets from another profitable company without a large subsidized loan from taxpayers. In this case, the Obama Administration is funding the KCS in its purchase of 30 new locomotives from GE. The Obama Administration has recently doubled-down on its backing of the US Ex-Im bank, which has been helping to fund Boeing aircraft sales to foreign airlines (each of which, surprise!, has a couple of GE engines on it).

GE knows how this political game is played, with resources allocated based on quid pro quo. Just the other day, GE announced that it would help bail out Obama and Government Motors buy mandating that all its company vehicles be Chevy Volts, in effect committing to buy more Volts than Chevy sold to consumers all last year. Of course, the circle has no end, so in turn GE will be rewarded with $90,000,000 in government subsidies for its 12,000 Chevy Volts, a number that could increase to $120 million if Obama's proposal to increase the per car subsidy is accepted.

By the way, the Obama Administration has criticized oil companies like Exxon-Mobil for earning excessive profits and getting overly large tax breaks. In 2010, Exxon paid a whopping 40.7% of its income in taxes ($21.6 billion in taxes on $53 billion in profits). In the same year, Obama subsidiary General Electric paid 7.4% of profits in taxes.

I accidentally watched a few minutes of a morning show today, something I try really hard to avoid. Matt whats-his-name was interviewing Richard Branson, and they were talking about the importance of corporations "doing good". Once startups get going, Branson said, they need to start doing good for people, meaning I guess that they buy carbon offsets or something.

Guess what? If my startup is succesful, I am already doing good. I can't make a dime unless I create value for people net of what they pay me. Every customer walks away from our interaction better off, or they would not have voluntarily elected to trade with me (and if they are not better off, I will never see them again and I will find lots of nasty stuff chasing future customers away on the Internet.) I am tired of this notion that a succesful business person's value can only be judged by what he or she does with their money and time outside of business. I understand the frustration with a few Wall Street and GE-type executives who are living like fat ticks on their connections with government, but most of us only are succesful if we do something useful.

This, from Carpe Diem, is along the same lines. He looks at an editorial from the DC paper about the entry of Walmart, which says among other things

Despite the peacocking by Gray and others after the agreement was signed, the District is receiving mostly crumbs. Walmart has committed to providing $21 million in charitable donations over the next seven years, an average of $3 million a year. That's a pittance."

Walmart does not have to do squat for the community beyond its core business, because selling a broad range of goods conviniently and at really low prices is enough. Or if it is not enough, they will not make money. The promise of $21 million to some boondoggle controlled by a few politician's friends is just a distraction, I wish they had not done it, but I understand that this is essentially a bribe to the officials of the DC banana republic to let them do business.

Postscript: I have no problem with doing charitable work outside of work. Both my company and I do, by choice, though unlike Richard Branson I don't need to have a crew of paid PR agents making sure everyone knows it.

Especially when the government is doing all it can to damp the forces of evolution and extinction. Via Mickey Kaus

Dysfunctional–or at any rate, not-functional-enough–corporate cultures are hard to change. That would include both the culture of the Old GM and that of many of its suppliers. Obama should have been more skeptical about “New GM’s” ability to turn itself around with its same old workforce and same old union

I warned of something similar long before GM was rescued by Bush and Obama:

But things change. Sometimes that change is slow, like a creeping climate change, or sometimes it is rapid, like the dinosaur-killing comet. DNA that was robust no longer matches what the market needs, or some other entity with better DNA comes along and out-competes you. When this happens, when a corporation becomes senescent, when its DNA is out of date, then its multiplier slips below one. The corporation is killing the value of its assets. Smart people are made stupid by a bad organization and systems and culture. In the case of GM, hordes of brilliant engineers teamed with highly-skilled production workers and modern robotic manufacturing plants are turning out cars no one wants, at prices no one wants to pay.

Changing your DNA is tough. It is sometimes possible, with the right managers and a crisis mentality, to evolve DNA over a period of 20-30 years. One could argue that GE did this, avoiding becoming an old-industry dinosaur. GM has had a 30 year window (dating from the mid-seventies oil price rise and influx of imported cars) to make a change, and it has not been enough. GM’s DNA was programmed to make big, ugly (IMO) cars, and that is what it has continued to do. If its leaders were not able or willing to change its DNA over the last 30 years, no one, no matter how brilliant, is going to do it in the next 2-3.

So what if GM dies? Letting the GM’s of the world die is one of the best possible things we can do for our economy and the wealth of our nation. Assuming GM’s DNA has a less than one multiplier, then releasing GM’s assets from GM’s control actually increases value. Talented engineers, after some admittedly painful personal dislocation, find jobs designing things people want and value. Their output has more value, which in the long run helps everyone, including themselves.

The alternative to not letting GM die is, well, Europe (and Japan). A LOT of Europe’s productive assets are locked up in a few very large corporations with close ties to the state which are not allowed to fail, which are subsidized, protected from competition, etc. In conjunction with European laws that limit labor mobility, protecting corporate dinosaurs has locked all of Europe’s most productive human and physical assets into organizations with DNA multipliers less than one.

My new column is up at Forbes, and it is one of my favorites I have written for a while (at least it seems so with my current scorpion-induced double vision). It begins with Krugman's recent statement that the Left understands the Right and libertarian positions better than the Right and libertarians understand the Left.

I first demolish this as a pretentious crock, but then wander to more important topics

But I do understand the leftish position well enough to identify its key mistake. As I mentioned earlier, we libertarians are similarly concerned with aggregations of power. We have, at best, a love-hate relationship with large corporations, for example, enjoying the bounties they can bring us but fearing their size and power.

But what the Left ignores is that there is absolutely no power imbalance as large as that between the government and its citizens. After all, you may get ticked off when Exxon charges you $4.00 a gallon for gas for reasons that aren't transparent to you, but you can always tell Exxon to kiss off and buy from someone else, or ride a bike, or stay home. Because Exxon does not have armies and police and guns and prisons.

Every single time we give the government the power to right a perceived imbalance, we give the government more power than the private entity we are trying to contain. In effect, we make things worse. Because we want the government to counter-act the power of oil companies, Congress now has the power to dump large portions of our food supply into motor fuel, to the benefit of just a few politically connected ethanol companies.

One of the reasons the Left often cannot adequately articulate the libertarian position is that the notion of bottom-up emergent order tends to be difficult for many to understand or accept (this is mildly ironic, since the Left tends to defend the emergent order of Darwinian evolution against the top-down Christian creation vision).

The key to much of libertarian economics is not that libertarians trust private actors, but that libertarians trust natural correction mechanisms in free markets far more than it trusts authoritarian power of the government. When, for example, large corporations become sloppy and abusive and senescent, markets will eventually bring them down.

In fact, when government is given power, nominally to correct such imbalances, they tend to use it to protect those in power as often as they do to protect the disenfranchised. Government restrictive licensing of hair dressers, interior designers, and morticians; bailouts of GM, Chrysler, and AIG; corporate welfare to GE and ADM; and use of imminent domain to hand private property to favored real estate developpers -- all are examples of finding government cures for perceived private power imbalances that are worse than the disease.

Isacc Asimov, in a book called Foundation that Paul Krugman recently rated as one of the most influential on his life, related this fable: Once there was a man and a horse, who were both imperiled by a wolf. The man approached the horse, and said that if the horse would put its superior speed at his disposal, he could kill the wolf. And so the horse agreed to take the man's saddle and bridle, and helped the man kill the wolf. The horse said, "great job, now remove your saddle and we can both be free," and the man said "never!"

I hope the moral of the story is clear. In trying to deal with the threat of the wolf, the horse gave the man so much power he became an even bigger threat. So too when we look to government to solve our problems.

Read the whole thing, as they say

Kevin Drum doesn't buy the regime uncertainty argument as a partial explanation of the slow recovery.

Here's what's remarkable: Carter, a law professor at Yale, apparently never once bothered to ask this guy just what regulations he's talking about. Is he concerned with general stuff like the healthcare law? Or something highly specific to his industry? Or what?

Regardless, I've heard this kind of blowhard conversation too often to take it seriously. Sure, it's possible this guy manufactures canisters for nuclear waste or something, and there's a big regulatory change for nuclear waste storage that's been in the works for years and has been causing everyone in the industry heartburn for as long as they can remember. But the simple fact is that regulatory uncertainty is no greater today than it's ever been. Financialuncertainty is high, but the Obama adminstration just hasn't been overhauling regs that affect the cost of new workers any more than usual. The only substantial exception is the new healthcare law, and if you oppose it that's fine. But it was passed over a year ago and its effects are pretty easy to project.

First, the costs of the health care law are NOT easy to project, and are made even harder when your company might or might not get waivers from certain provisions. Second, he seems to forget cap and trade, first by law and then by executive fiat; the NLRB's new veto power over corporate relocations it exercised with Boeing; the absurdly turbulent tax/regulatory/permitting regime in the energy field, and particularly oil and gas. How about trillion dollar stimulus projects, that until very recently Obama was still talking about replicating (and Krugman begs for to this day). I could go on and on. This is spoke just like a person who never had to run a business.

Further, I wrote this in the comments section:

I think you are both right and wrong. I am sure the discussion about this is to some extent overblown. But you are thinking about business and hiring much too narrowly.

You seem to have a mental model of business showing up at the door, and someone turning that business down because they don't want to hire an employee to serve it (or out of sheer petulance because Fox News told them to sit on their hands, lol). You find it unlikely anyone would refuse the business, and so do I.

But I run a small to medium size business, and a lot of hiring decisions don't work that way. I do have some situations that fit your model - I have a campground that is really busy this year, so we hired more people to serve the volume. No problem.

But most of my hiring decisions are effectively investments. I am going to create a new position, pay money to train that person, and pay their wage for a while in advance of demand. Or I am going to open a new site or department or location and make a lot of investment, and the return on investment may be very sensitive to small changes in labor or regulatory costs.

For our business, with labor costs over 50% of costs, the issue is definitely labor costs. Our pre-tax margins are in the 6-7% range. So if labor costs are 60% of revenues, then a 10% change in labor costs might wipe out the margin entirely, and a much smaller change in costs might flip the investment from making sense to not making sense.

We run a seasonal business with part-time workers who are older and on Medicare. Regulations about exactly how much we will have to pay under Obamacare have not been written, so we have no idea how much our employment costs will go up in 2014, so we sit and wait. I have cancelled two planned campground construction projects in the last 6 months because we have no freaking idea if they will make money.

If I am having trouble with just this one law figuring out whether to make investments, what are, say, oil companies doing in evaluating investments when they have absolutely no idea what their taxes will be, whether they will be permitted or not to drill, or whether they will be subject to cap and trade?

One other thought, it strikes me that there is a lot of good scholarship that suggests that the Great Depression was extended by just this kind of regime uncertainty. Now, of course, the proposed structural changes to the economy being proposed at the time were more radical than anything on the table today. The National Industrial Recovery Act was essentially an experiment in Mussolini-style economic corporatism, until most of it was struck down by the Supreme Court. Nothing so radical is being proposed (unless you work in health care).

Look, I know the Left has convinced itself that only consumer demand matters in an economy, but business investment has simply got to matter in a recovery. If the returns on future investments are harder to predict, and therefore riskier, businesses are going to apply a higher hurdle rate to new investments, meaning they don't stop entirely, but do invest less.

One interesting may to confirm this some day would be to look back and see if larger corporations with political access invested more than smaller ones or ones with less access. Did GE, who clearly can get whatever it wants right now from the government, invest more than a small company or even than Exxon, which is on the political outs? If so, this in my mind would confirm the regime uncertainty hypothesis, because it means that the companies doing most of the investing were the ones confident that they could shape the mandates coming out of the government in their favor.

Beyond regime uncertainty, if you want to talk about Obama and the recovery, you have to mention that a trillion dollars was diverted from private hands to public hands. Does anyone believe that taking a trillion dollars out of whatever investments private actors would have used the money for and diverting most of it to help maintain government payrolls is really the way to increase the strength and productivity of the economy?

I have to take this with a grain of salt, because it is coming from GE, the current American poster-child for rent-seeking, particularly in attempting to be a magnet for green energy subsidies. But since the statement can be seen as under-cutting the subsidy argument, I have to take it more seriously:

Solar power may be cheaper than electricity generated by fossil fuels and nuclear reactors within three to five years because of innovations, said Mark M. Little, the global research director for General Electric Co.

“If we can get solar at 15 cents a kilowatt-hour or lower, which I’m hopeful that we will do, you’re going to have a lot of people that are going to want to have solar at home,” Little said yesterday in an interview in Bloomberg’s Washington office.

....GE, based in Fairfield, Connecticut, announced in April that it had boosted the efficiency of thin-film solar panels to a record 12.8 percent....The cost of solar cells, the main component in standard panels, has fallen 21 percent so far this year, and the cost of solar power is now about the same as the rate utilities charge for conventional power in the sunniest parts of California, Italy and Turkey.

I am all for that. I have always had faith that solar would make sense someday, and that we would be ranking out cheap solar conversion surfaces like carpet out of Dalton, Georgia, but every time I have priced it to date on my house, even with huge government subsidies, it has not made sense. In Europe, it requires 50-60 cent feed in tariffs (basically a subsidy in the form of above-market electricity prices paid by the utility for solar-sourced electricity) to get solar capacity installed, so 15-cents would be great and is approaching the cost of electricity in some high cost areas.

Here in Phoenix, FirstSolar does a ton of thin film. I have always had mixed feelings about FirstSolar. On the one hand, they live off subsidies and would basically not be in business if it were not for huge European subsidies of various forms. On the other, though, they have been one of the few solar companies that actively have talked for years of a development path to a cost position that does not require subsidies.

This is the kind of story I always thought typical of corporate states like France. It is sad to see this happening so frequently in the US

Recently, President Obama selected General Electric CEO Jeffrey Immelt to chair his Economic Advisory Board. GE is awash in windmills waiting to be subsidized so they can provide unreliable, expensive power.

Consequently, and soon after his appointment, Immelt announced that GE will buy 50,000 Volts in the next two years, or half the total produced. Assuming the corporation qualifies for the same tax credit, we (you and me) just shelled out $375,000,000 to a company to buy cars that no one else wants so that GM will not tank and produce even more cars that no one wants. And this guy is the chair of Obama's Economic Advisory Board?

This is the classic kind of cozy relationship between large industrial corporations and government that has been a feature of European states for years.

This story is from the WSJ, and gets extra bonus points for including the poster-boy of the corporate state, Jeffrey Immelt

Treasury and OMB singled out an 845-megawatt wind farm that the Energy Department had guaranteed in Oregon called Shepherds Flat, a $1.9 billion installation of 338 General Electric turbines. Combining the stimulus and other federal and state subsidies, the total taxpayer cost is about $1.2 billion, while sponsors GE and Caithness Energy LLC had invested equity of merely about 11%. The memo also notes the wind farm could sell power at "above-market rates" because of Oregon's renewable portfolio standard mandate, which requires utilities to buy a certain annual amount of wind, solar, etc.

But then GE said it was considering "going to the private market for financing out of frustration with the review process." Anything but that. The memo dryly observes that "the alternative of private financing would not make the project financially non-viable."

Oh, and while Shepherds Flat might result in about 18 million fewer tons of carbon through 2033, "reductions would have to be valued at nearly $130 per ton CO2 for the climate benefits to equal the subsidies (more than 6 times the primary estimate used by the government in evaluating rules)."

So here we have the government already paying for 65% of a project that doesn't even meet its normal cost-benefit test, and then the White House has to referee when one of the largest corporations in the world (GE) importunes the Administration to move faster by threatening to find a private financial substitute like any other business. Remind us again why taxpayers should pay for this kind of corporate welfare?

First, the moment GE said that this could be financed privately, the Feds should have said "then what the f*ck are you talking to us for? Get out of here." By the way, privately probably does not mean privately -- it probably means going to private banks or investors who in turn access many of the same taxpayer funds.

Second, its amazing that the threat to finance this privately rather than sponging off taxpayer funds is treated as a threat by the Obama Administration. They desperately want to "take credit" for the project and can only do so by spending our money (this is the same impulse that propels politicians who have never given a dime to charity to want to spend taxpayer money in order to be called "caring.")

Supporters of Obamacare argued that it would reduce costs because decisions to fund or not fund certain procedures and drugs would be left to panels of experts (later derisively labelled "death panels").

I have argued many times that these panel's job is hopeless. Solutions and products that may be right for one person may be a waste for another situation, and there is absolutely no way they have the information or the scope to make decisions with any kind of granularity. One-size-fits-all solutions result.

But let's hold that thought for a minute. Let's presume that these supposedly non-political boards will make near-perfect decisions. Then what? Those decisions become the law of the land?

Hah. We have a parallel situation in the military, where DoD procurement supposedly acts as the disinterested expert, which Congress frequently ignores to pay off various constituencies.

If Congress is looking for New Year's resolutions, it could start by breaking the habit of funding programs the government doesn't want. A case in point is the attempt to throw another $450 million at the development of a second engine for the F-35 Joint Strike Fighter, a plan that Defense Secretary Robert Gates says the military doesn't need.

In what has become an annual ritual, Congress is weighing whether one of the largest weapons programs in history should support the development of F-35 engines by both General Electric and Pratt & Whitney. In 2001, GE's engine lost in the procurement competition to the one designed by Pratt & Whitney, as F-35 developers Lockheed Martin and Boeing preferred the latter version.

To hedge its technological risk, the Pentagon nonetheless sought financing for the GE engine as a backup through 2006 in case the Pratt & Whitney version fell short. That hasn't happened, and as budgets have tightened the Pentagon has understandably decided that it needs only one engine design. As Secretary Gates put it, "Only in Washington does a proposal where everybody wins get considered a competition, where everybody is guaranteed a piece of the action at the end."

The Pentagon's opposition hasn't stopped Congress, where the usual parochial suspects are still stumping for GE. And the White House appears to be bending.

Of course they are -- the GE CEO carried a lot of water for Obama on health care and energy policy, and will be expecting a pay back. Someone has to be terribly naive to believe similar shenanigans won't take place with health care.

But we don't have to wait to test this hypothesis. The fifty states all have must-carry rules in their states, which have a lot more to do with political pull than science - more here and here.

As can be expected, the media really did a poor job of covering the GM IPO, consistently underestimating the total public cost of the bailout (e.g. no one is mentioning the $45 billion in tax-loss carryforwards GM was allowed to keep, against all precedent).

But the real cost of the handling of the GM bankruptcy is in 1) the terrible precedents it set in hammering secured creditors to the benefit of favored political allies of the Administration and 2) the loss of the opportunity to get billions of dollars in production assets out of the hands of the people who have be sub-optimizing them.

It was this latter issue I have focused the most on, particularly in this post where I argued for letting GM die. I said in part:

All these management factors, from the managers themselves to process to history to culture could better be called the corporate DNA. ...

Corporate DNA acts as a value multiplier. The best corporate DNA has a multiplier greater than one, meaning that it increases the value of the people and physical assets in the corporation. When I was at a company called Emerson Electric (an industrial conglomerate, not the consumer electronics guys) they were famous in the business world for having a corporate DNA that added value to certain types of industrial companies through cost reduction and intelligent investment. Emerson's management, though, was always aware of the limits of their DNA, and paid careful attention to where their DNA would have a multiplier effect and where it would not. Every company that has ever grown rapidly has had a DNA that provided a multiplier greater than one"¦ for a while.

But things change. Sometimes that change is slow, like a creeping climate change, or sometimes it is rapid, like the dinosaur-killing comet. DNA that was robust no longer matches what the market needs, or some other entity with better DNA comes along and out-competes you. When this happens, when a corporation becomes senescent, when its DNA is out of date, then its multiplier slips below one. The corporation is killing the value of its assets. Smart people are made stupid by a bad organization and systems and culture. In the case of GM, hordes of brilliant engineers teamed with highly-skilled production workers and modern robotic manufacturing plants are turning out cars no one wants, at prices no one wants to pay.

Changing your DNA is tough. It is sometimes possible, with the right managers and a crisis mentality, to evolve DNA over a period of 20-30 years. One could argue that GE did this, avoiding becoming an old-industry dinosaur. GM has had a 30 year window (dating from the mid-seventies oil price rise and influx of imported cars) to make a change, and it has not been enough. GM's DNA was programmed to make big, ugly (IMO) cars, and that is what it has continued to do. If its leaders were not able or willing to change its DNA over the last 30 years, no one, no matter how brilliant, is going to do it in the next 2-3.

So what if GM dies? Letting the GM's of the world die is one of the best possible things we can do for our economy and the wealth of our nation. Assuming GM's DNA has a less than one multiplier, then releasing GM's assets from GM's control actually increases value. Talented engineers, after some admittedly painful personal dislocation, find jobs designing things people want and value. Their output has more value, which in the long run helps everyone, including themselves.

The alternative to not letting GM die is, well, Europe (and Japan). A LOT of Europe's productive assets are locked up in a few very large corporations with close ties to the state which are not allowed to fail, which are subsidized, protected from competition, etc. In conjunction with European laws that limit labor mobility, protecting corporate dinosaurs has locked all of Europe's most productive human and physical assets into organizations with DNA multipliers less than one.

The NY Times has a fairly ugly story, though hardly unique, of a project to restore water flow to the Everglades turning into a corporate welfare project for United States Sugar. The short story is that in a time when United States Sugar was in desperate financial straights and when real estate prices in Florida were tumbling, the Florida government treated USS like it had all the power, rolling over to paying above-market prices and letting USS pick and choose the land parcels to be purchased. The story did not mention much about it, but there is a second large sugar producer in the area who it strikes me could have been played off against USS to get the best deal.

Remember that the US Sugar operation likely exists only because of sugar tariffs and import quotas that raise the price of sugar in the US well above the world norm. So consumers are paying extra, and drinking soft drinks with crappy HFCS, so that US Sugar can screw up the Everglades and get bailed out by taxpayers. Readers will understand it is the purest coincidence that US Sugar's attorney is chief of staff to the state's governor.

From running my recreation privatization blog, I know that there are many folks who will ascribe this to a failure of private enterprise and an excess of corporate speech and money in politics. But to my mind this is a great example of why election and speech limits don't have any utility. This is all back room lobbying, cronyism, and quid pro quo politics that doesn't show up in any monetary ledger, and thus are not and have never been subject to any limits. As I wrote here:

when the stakes of government are so high, money and influence never goes away. Just as in any economy, when you ban money, a barter economy arises. So if we ban large campaign spending, then the quid pro quo becomes grass roots efforts and voter mobilization. Groups like the UAW become more powerful (we are seeing that already). They are trading their member's votes for influence. Connected companies like GE are doing the same thing, trading their support for legislation that is generally hostile to commerce for specific clauses in said legislation that exempts GE and/or makes the laws even more punishing on their competition. The problem with all this activity is it is hard to see and totally unaccountable "” at least with advertisements we see people out in the open with their agendas.

The other obvious point is that no private entity would ever allow themselves to get rolled so badly by US Sugar. They would have sense USS's weakness and broken its knees in the negotiation. One US Sugar manager even says as much:

For its board members, Mr. Crist's overture was appealing in part because they figured a government purchase would be far more lucrative than a private deal.

"It wasn't another company coming in and bottom-fishing you," Mr. Wade said. "They knew it would be for fair-market appraisals."

Over at my privatization blog, I wrote about a deal in Chicago where the government made four or five huge mistakes in issuing a private contract that a private company (or at least one that is not going to go bankrupt) would never make. So of course the problems are blamed on privatization.

I had a dinner conversation last night with my Massachusetts mother-in-law. She is pretty interesting to talk to because she is a pretty good bellwether for Democratic talking points on most issues. She was opposed to the recent Supreme Court speech decision removing limits on third party advertising near an election (I think she misunderstood the scope of that decision but that is not surprising given the shoddy reporting on it, up to and including Obama getting it wrong in his State of the Union). She advocated strict campaign spending restrictions (both in terms of amount of money and length of the campaign season) combined with term limits.

We could have gone a lot of places with the discussion, but we ended up (before we terminated the conversation in the name of civility) discussing whether restrictions on money were equivalent to restrictions on speech. She of course said they were not, and said under strict monetary controls I still had freedom of speech - weren't we still talking in the car?

It is hard to reach common ground when one person is arguing from a strict rights-based point of view while the other is arguing from a utilitarian point-of-view. Essentially she knows in her heart that she is restricting speech, but wishes to do so to reach a better outcome. I made a couple of utilitarian arguments, including:

However, I tend to shy away form utilitarian arguments. The best arguments I have against the notion that money can be restricted without restricting speech are:

A friend of mine from Princeton days writes:

... and you seem in favor of the Supreme Court decision in Citizens United vs the FEC, I was wondering how you feel about being a customer or supplier or competitor of large businesses who can spend far more than your business to influence the rules of the game.

From what I read, I am sure you have a compelling answer, but I would be scared to death. (Maybe that's why I work for a large corporation [Target] instead of attempting to run my own business.)

I thought this was a pretty good question, and I answered:

- I try hard not to make utilitarian arguments to Constitutional and rights issues. As an example, I am sure we might have less crime if the police were empowered to incarcerate anyone they wanted without trial, but we don't do it that way.

- I worry most about corporate lobbying (e.g. by Immelt at GE) and this is unaffected by this ruling - it was legal before and after. This decision allows corporate advertising, which is public and visible, which I can at least see and react to, as opposed to back room deal making.

- Libertarians certainly worry about your question, and why many of us fear that what we are creating in this country is a European-style corporate state, rather than socialism. To a libertarian, the answer is not less speech, but less government power to pick winners and losers in commerce.

{kind=link}