I Love SpaceX But Hate Its Proposed IPO

I have been recuperating from some health issues and have not been writing much, but I really don't want to miss out on putting my oar in the water prior to the SpaceX IPO. As background, I love to watch what SpaceX is doing in launch and believe they have made a huge contribution to the world in doing so. As a former operator of hundreds of wilderness campgrounds, Starlink was the greatest single new technology for our business in 20 years. But you don't automatically get your way with stock valuations just because what you do is cool and useful -- there has to be some prospect of making back the investment.

Anyone who has been following Tesla for years has to know what is coming at SpaceX. In the movie Gettysburg, the great Sam Elliot speaks these lines as General Buford, the union Cavalry commander who was able to slow the southerners just enough on day 1 to let the Union grab the high ground. But ahead of this success, he fears that he and the union will fail and the South would slaughter Union troops trying to take the hills too late, as at Fredericksburg (and as happened to Pickett a couple days later).

Devin, I've led a soldier's life, and I've never seen anything as brutally clear as this. It's as if I can actually see the blue troops in one long, bloody moment, goin' up the long slope to the stony top. As if it were already done... already a memory. An odd... set... stony quality to it. As if tomorrow has already happened and there's nothin' you can do about it. The way you sometimes feel before an ill-considered attack, knowin' it'll fail, but you cannot stop it. You must even take part, and help it fail.

Having been a (peripheral) part of the online community skeptical of Tesla stock valuation, I feel I can see the future of SpaceX stock over time as if it has already happened.

There are at least two distinct patterns one sees over time in the stock of Musk-led Tesla that I fully expect to see duplicated at SpaceX. So it is worth reviewing those.

1. Absurd Valuation Based on Musk Shouting "Squirrel"

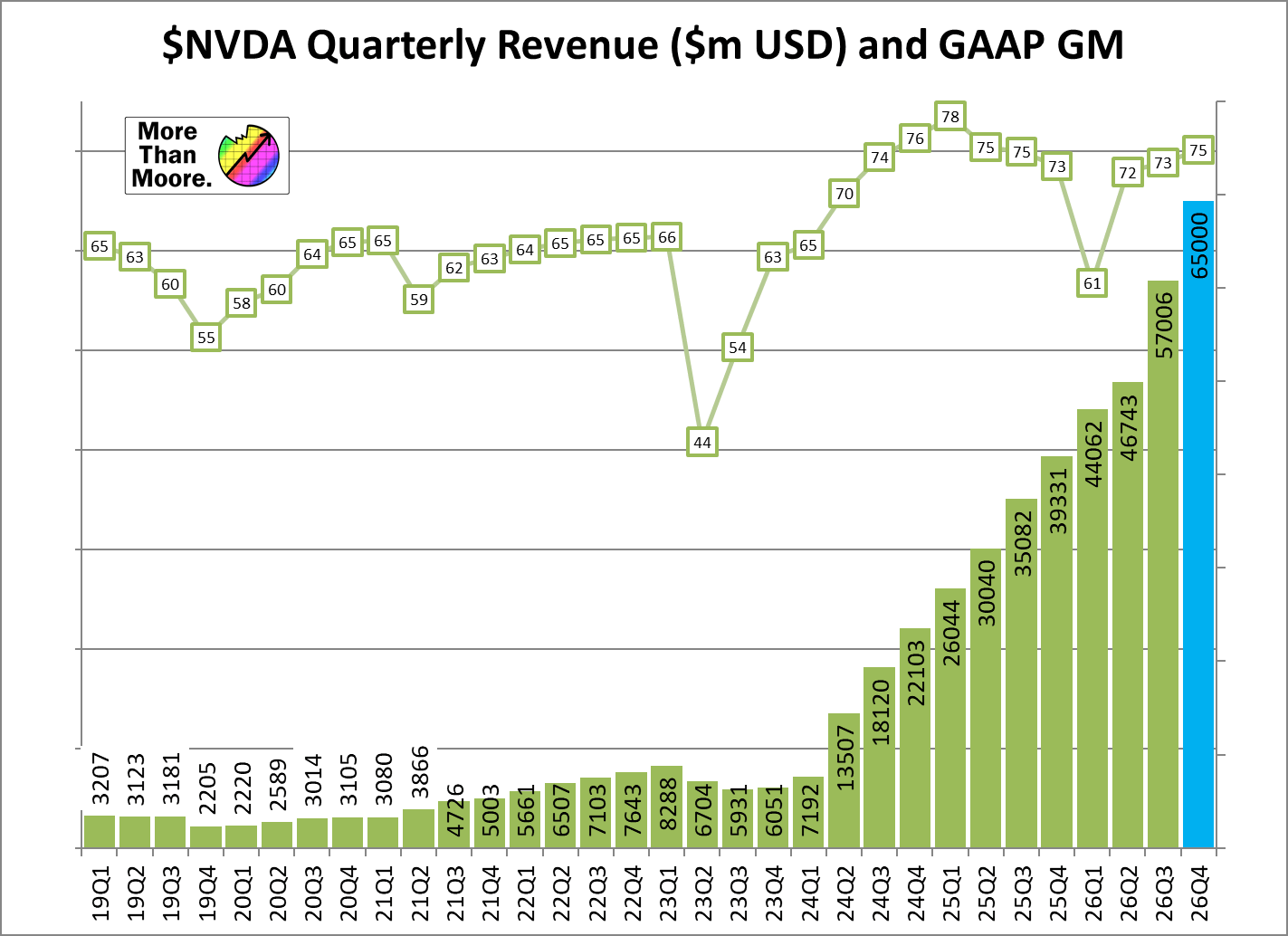

Tesla has a Trailing 12 Month PE ratio of 387(!) and a forward PE of 216. These ratios are almost unprecedented for a company not in the middle of a restructuring, and indicate simply enormous growth expectations. This is not some weird temporary data spike... Tesla has maintained a PE over 150 for years and years. Just to give it context, let's compare it to Nvidia which is perhaps the world's most famous growth company right now. Nvidia's revenues have really gone vertical over the last quarters:

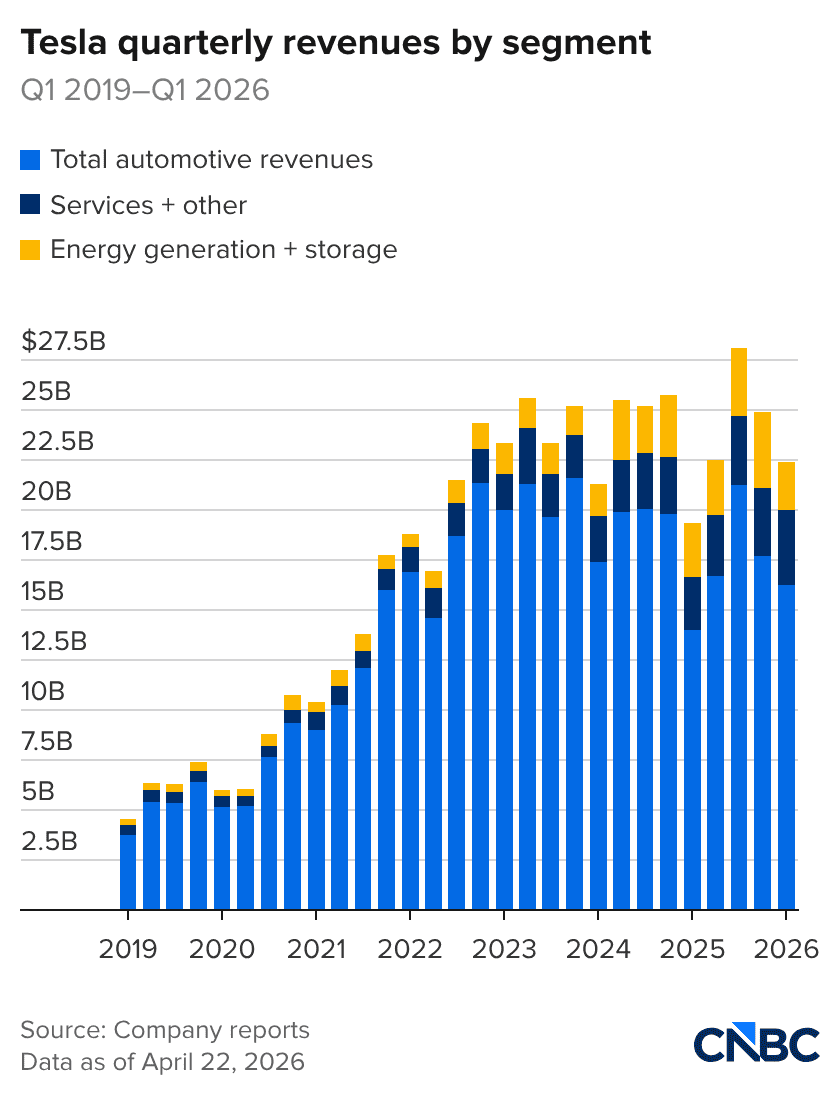

For that it has been rewarded with a PE of 34 / 25 (Trailing / Forward). So Tesla must REALLY be growing to justify a PE of nearly 400, right? Well, not really. In fact, Tesla's revenue has been essentially flat for 14 quarters:

So how does Tesla maintain such a crazy-high valuation? Honestly, I don't know. But from watching it and Musk for years I would argue that the most important factor has been Musk's ability to keep shifting the endgame. The response to valuation concerns is always "yeah, but you are only looking at the current business, [fill in the blank] which is coming soon[-ish] will be worth a trillion dollars." The fill-in-the-blank over the years has included solar roofs, full self-driving, semi-trailers, battery swap, robo-taxis, neural implants, humanoid robots, and AI.

Tesla Translated to SpaceX: The proposed SpaceX valuation of $1.75 trillion is, if anything, even crazier than Tesla's. It is impossible to apply a PE, since SpaceX loses money and can be expected to do so for years, even decades. But with about $18.7 billion in revenue last year, the SpaceX valuation is nearly 100x revenue (Tesla trades at a lofty 15x revenue). Nobody, ever, has made money investing in a 20-year-old company with low margins at 100x revenue (barring the occasional sucker who will later pay 120x).

The tell for me is the emphasis and investment in AI at SpaceX. Strategically, this is a terrible idea as their core business is already very capital intensive and they really don't need a diversion into something else. They are competing in AI with a number of companies that are far ahead of them and I don't see an obvious way to catch up (very similar to Tesla and self-driving). Musk says they are ahead but Musk said Tesla was ahead on self-driving and robotaxis until it has become obvious that they are not even close. There is a potential AI-related launch and hardware opportunity, maybe, someday, to put AI processing in space, but there is no reason that should be dependent on SpaceX's independent investments in AI. The one thing AI gives SpaceX, of course, is a squirrel to help fill in the value hole between "losing money on $18 billion of revenue" and $1.75 trillion. Investors in SpaceX can expect a constant stream of squirrels over the coming years.

2. Propping Up Older Musk Investments with Newer Ones

Over the years of following Musk, the one action of his that aggravated me more than anything else was the transparent bailout of his friends' and family's investment in SolarCity using Tesla stock. Like most other rooftop solar businesses, in 2016 SolarCity was close to bankruptcy. Rather than allowing that to happen, losing money and prestige for Musk, Musk used his extraordinary control of the Tesla board to have Tesla buy out SolarCity for far more than any sensible market value. In doing so, Musk trumpeted another classic Tesla squirrel, presenting the Solar Roof, basically modular rooftop solar tiles that looked like wood or slate that would snap together into an attractive rooftop installation. It was later found that most of the early demo was likely fake, as the tiles were not even close to release-ready and while Musk was predicting 12,000 installations per year and growing, perhaps only 3000 in total were ever completed over 10 years. The Solar City results continued to fall at Tesla and were rapidly buried in the energy sector, making it almost impossible to figure out how much value Tesla got from SolarCity, given that the vast majority of energy sector revenues are unrelated to rooftop solar and are instead large battery storage projects.

Since that time Musk has used his AI lab xAI to buy Twitter/X. And then just this year had SpaceX buy xAI for $250 billion. Does it make sense that an orbital launch company own a social media platform? Absolutely not, but it bailed Musk out of an investment in X that was going to be very hard to ever recover any other way.

Tesla Translated to SpaceX:

Last year Tesla booked $890 million in revenue from SpaceX (cars, battery storage, some AI). This is less than 1% of Tesla's revenues though I expect it to be, since it was not arms length, more profitable than average. But the real threat to SpaceX will be, as Tesla's stock valuation eventually starts to return to Earth, that Musk will use his unique control of both companies to have SpaceX buy Tesla. People are already discussing it. These are two companies that absolutely have no reason to be under one roof EXCEPT that it would help maintain Musk's net worth. Yes, I am sure he will generate a logic that the Musk fan-boys will love -- AI consolidation or some such. And I guess it would be accretive, in an ugly way, with a 100x revenue company buying out a 15x. Just remember that these two companies, which if the IPO price holds for SpaceX, have a combined market cap of $3 trillion and a combined 2025 net income of -$1 billion. Even if your excel spreadsheet has enough columns to add years marching towards the heat death of the universe, I am not sure that investment ever pays off.

Parting Thoughts

None of this necessarily means that the SpaceX IPO will fail or that SpaceX stock won't rise post-IPO. I spent too many years getting burned off and on shorting Tesla to ignore the fact that any Musk enterprise commands a premium among a subset of investors -- he is like Warren Buffet in that his name association with a deal has overwhelming value (the only difference from Buffet being that Buffet's investments actually produce profits). Be aware if you invest that you are likely soon to own Tesla as well, because I do not think Musk can resist the temptation to use high-multiple SpaceX stock as wampum to buy out his other investments.

There is a sort of clock in Musk investments, going back to SolarCity. There is a lot of arm-waving and squirrels to maintain a valuation, but as business performance inevitably does not live up to the valuation hype, its time to have the next investment that is at the peak of its hype with a huge multiple buy out the old one. I really thought Tesla might finally hit that point when the valuation collapses to that of a low-growth car company once the robotaxi initiative proved a loser, but here comes SpaceX just in time.

I do not give out investment advice but if I were short Tesla right now I would run for my life. The SpaceX IPO will essentially be a big Tesla bailout.

{kind=link}