Are You Desperately Worried About Global Warming? Then You Should Be Begging for More Fracking

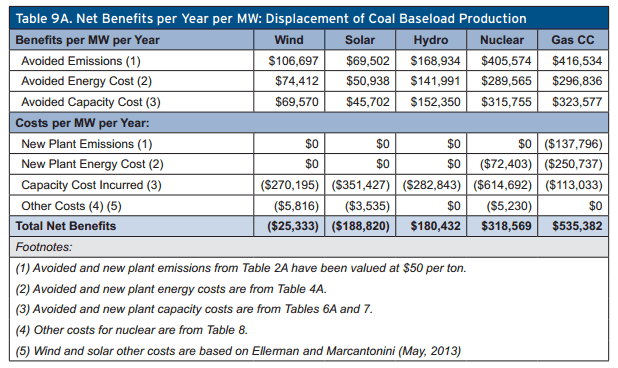

Charles Frank of Brookings has looked at the relative returns of various energy investments in the context of reducing CO2. The results: The best answer is natural gas, with nothing else even close. Solar and Wind can't even justify their expense, at least from the standpoint of reducing CO2. Here is the key chart (Hat tip Econlog)

Note that this is not a calculation of the economic returns of these types of power plants, but a relative comparison of how much avoided costs, mainly in CO2 emissions (valued at $50 per ton), there are in switching from coal to one of these fuel sources. Natural gas plants are the obvious winner. It remains the winner over solar and wind even if the value of a ton of CO2 is doubled to $100 and both these technologies are assumed to suddenly get much more efficient. Note by the way that unlike wind and solar (and nuclear), gas substitution for coal plant yields a net economic benefit (from reduced fuel and capital costs) above and beyond the avoided emissions -- which is why gas is naturally substituting right now for coal even in the absence of a carbon tax of some sort to impose a cost to CO2 emissions.**

I was actually surprised that wind did not look even worse. I think the reason for this is in how the author deals with wind's reliability issues -- he ends up discounting the average capacity factor somewhat. But this understates the problem. The real reliability problem with wind is that it can stop blowing almost instantaneously, while it takes hours to spin up other sorts of power plants (gas turbines being the fastest to start up, nuclear being the slowest). Thus power companies with a lot of wind have to keep fossil fuel plants burning fuel but producing no power, an issue called hot backup. This issue has proved itself to substantially reduce wind's true displacement potential, as they found in Germany and Denmark.

There is no evidence that industrial wind power is likely to have a significant impact on carbon emissions. The European experience is instructive. Denmark, the world's most wind-intensive nation, with more than 6,000 turbines generating 19% of its electricity, has yet to close a single fossil-fuel plant. It requires 50% more coal-generated electricity to cover wind power's unpredictability, and pollution and carbon dioxide emissions have risen (by 36% in 2006 alone).

Flemming Nissen, the head of development at West Danish generating company ELSAM (one of Denmark's largest energy utilities) tells us that "wind turbines do not reduce carbon dioxide emissions." The German experience is no different. Der Spiegel reports that "Germany's CO2 emissions haven't been reduced by even a single gram," and additional coal- and gas-fired plants have been constructed to ensure reliable delivery.

Indeed, recent academic research shows that wind power may actually increase greenhouse gas emissions in some cases, depending on the carbon-intensity of back-up generation required because of its intermittent character.

** Postscript: The best way to read this table, IMO, is to take the net value of capacity and energy substitution and compare it to the CO2 savings value.

![]()

The first line is just from the first line of the table above. The second is essentially the net of all the other lines.

I think this makes is clearer what is going on. For wind, we invest $106,697 for $132,030 $132,030 for $106,697 in emissions reduction (again, I think the actual number is lower). In Solar, we invest $258,322 for $69,502 in emissions reduction. For gas, on the other hand, we have no net investment -- we actually have a gain in these other inputs from the switch -- and then we also save $416,534. In other words, rather than paying, we are getting paid to get $416,534 in emissions reduction. That is not several times better than Solar and Wind, it is infinitely better.

Postscript #2: Another way to look at this -- if you put on a carbon tax in the US equal to $50 per ton of CO2 that fuel would produce, then it still likely would make no sense to be building wind or solar plants unless there remained substantial subsidies for them (e.g. investment tax credits, direct subsidies, guaranteed loans, above-market electricity pricing, etc). What we would see is an absolute natural gas plan craze.

{kind=link}