As always, take this with a grain of salt given my past history of investment advice. I am frequently correct on my calls to short something, but tend to be really early, such that a person (ie me) can likely be short-squeezed into oblivion before the fall takes place.

That being said, I think autos would be a good short. Why?

They are riding positive sentiment, based on a strong October. But October was strong because it had 5 weekends rather than 4 and recent results reflect a lot of channel stuffing. Shorting means finding the top, and this feels like the top

I would be stunned if the Volkswagen emissions cheating is limited to Volkswagen. Volkswagen is not unique -- Cat and I think Cummins were busted a while back for the same thing. US automakers don't have a lot of exposure to diesels (except for pickup trucks) but my guess is that something similar was ubiquitous. **

Apparently, the recent rebound in auto sales has been driven by a huge spurt of sub-prime lending that looks remarkably similar to the housing market 7 years ago:

This comes against a backdrop of rising US auto sales (see the numbers for October, out earlier today) and it's not difficult to explain the gains. Just take a look at the following data from Experian on the lunatic loan terms being extended to borrowers (from Q1):

Average loan term for new cars is now 67 months — a record.

Average loan term for used cars is now 62 months — a record.

Loans with terms from 74 to 84 months made up 30% of all new vehicle financing — a record.

Loans with terms from 74 to 84 months made up 16% of all used vehicle financing — a record.

The average amount financed for a new vehicle was $28,711 — a record.

The average payment for new vehicles was $488 — a record.

The percentage of all new vehicles financed accounted for by leases was 31.46% — a record.

** Postscript: The biggest problem with the emission cheating is that it caused the world to under-estimate the cost of emissions mandates. When performance of cars starts to drop noticeably when emissions cheating is fixed, it will be an eye-opener

A common thread running through the tens of thousands of emails that landed in Hillary Clinton’s in-box in her time as secretary of state is that aides and assorted advisers believe she is, well, awesome.

With a few exclamation points tacked on.

In notes sent to the private email account Mrs. Clinton used, various advisers routinely heap praise on the person who gave them their jobs or elevated them to her inner circle. Email flattery of this sort is a common tactic in the everyday workplace, but the Clinton emails show how it comes into play at the highest levels of government.

Employees tell Mrs. Clinton she is doing a “spectacular job,†that she has many admirers and that her remarks were “pitch perfect.†They assure her she looks “gorgeous†in photos and commend her clothing choices.

Look, I guess everyone has their own leadership style but from my experience it is a terrible idea to promote this kind of thing in one's organization.

Why? Well, my organization has 350 people in it. We can either think with just one person (me), working to improve our operations, or we can think with 350. Those 349 other people know many of the ways in which we are screwing up and can improve -- the problem is getting them to come forward with those ideas. And getting them to do so is far less likely if we are maintaining some sort of North Korean style personality cult of the CEO.

I have written about this before, but it's why I consider my Ivy League degrees to be a negative in running the company. Many of my employees have only a high school education (at best) and are intimidated in bringing up an idea or telling me I am screwing up because they assume since I have these Ivy League degrees I must be smarter than they are and know what I am doing. But in their particular job, in terms of my knowledge of what they see every day from customers and operationally, I am dumb as a post and completely ignorant.

Anyone who has worked for me for more than a few months can likely quote my favorite line which I use in most of my employee talks -- "If you see something that seems screwed up, don't assume Warren is smarter than you and wants it that way, assume that Warren is screwing up and needs to be told."

Postscript: This sort of flattery also makes me deeply uncomfortable on a personal level, so much so I have a hard time understanding people who revel in it. I once had an employee that could not stop with this sort of personal flattery, and eventually we ended up terminating them. We terminated them for other good reasons, but I must admit to being relieved when they left.

YP is the modern name for what used to be the Yellow Pages. Obviously, yellow pages are a dying business. Ten years ago the Phoenix Yellow Pages had to be broken up into two books, each a couple inches think. I happened to see one the other day, and it was the size of a short novel. They tried to move to the web, but who goes to Yp.com (vs. google or Yelp) to find a business?

Even in the glory days of yellow pages, it was always hard to cancel their service. If you did not tell them by like August, they would start billing you for the next year and sic a collection agency on you if you disputed it.

However, it appears that now that YP is a dying business, and knows that each lost customer will likely never be replaced, it has turned into the Hotel California.

In 2013, I left a location in Ventura County. We had advertised in the Yellow Pages for years (back when it made sense) and had never been able to cancel it in time -- by the time we remembered it each year it had already auto renewed. Soon after we left, I notified them that we needed to cancel. At the time, I tried to negotiate a reduction in the 2014 charges but figured I probably would have to pay them, which I did.

Then, in 2015 I started getting bills. I called each month patiently explaining and sending letters that we had already cancelled. They would say that they had no record of my ever calling, but they swore they would mark the account as closed and that it would be fixed. Then the next month it would all repeat -- a bad customer service Groundhog Day.

Finally this week I started getting legal threats and collection agency notices that I owe $499 for 2015 and that my life would be left in ruins with the ground salted if I did not pay immediately. So I called today and AGAIN they had no record of my cancelling -- in fact, it was on a path to renew again for 2016.

Look, I am the first to tell folks to never chalk up to conspiracy what can as easily be explained by mass incompetence. But at some point one has to suspect there is fraud going on here to retain customers as long as possible for a dying service.

So here is what I am left with -- I found someone in their organization who may be willing to settle my non-debt for non-services for a couple of hundred. I told them this was absurd, since I did not owe it, but that I would pay a couple hundred dollars if they would give me a letter that said the account is closed and fully settled. From the outside, this may seem a bad trade. But I have enough lawyers in my life and hiring lawyers would be the only way to solve this any other way. And besides, $200 is cheap compared to the thousands of dollars of my personal time I have spent farting with this.

Update 9/27/15: God, this is Groundhog Day! YP said that I should send a certified letter to such and such address to make absolutely sure that my account was cancelled. I sent it to that exact address, braving a 30-minute line at the post office to do so. So of course, the letter just came back undeliverable. I have held off saying this, but these guys are total scam artists. They seem to have no intention of ever letting me leave.

John Scalzi tries to explain privilege to non-SJW-types by saying that being a white male is like playing life on "easy" difficulty.

I'll grant I benefited from a lot of things growing up others may not have had. I had parents that set high standards, taught me a work ethic, taught me the value of education, had money, and helped send me to Ivy League schools (though the performance there, I would argue, was all my own).

Well, for those of you concerned about living down a similar life of privilege, I have a solution for you: start a business. Doing so instantly converted me into a hated abused underclass. Every government agency I work with treats me with a presumption of guilt -- when I get called by the California Department of Labor, I am suddenly the young black man in St. Louis called out on the street by an angry and unaccountable cop**. Every movie and TV show and media outlet portrays me as a villain. Every failing in the economy is somehow my fault. When politicians make a proposal, it almost always depends on extracting something by force from me -- more wages for certain employees, more health care premiums, more hours of paperwork to comply with arcane laws, and always more taxes.

Postscript: I will add an alternative for younger readers -- there is also a way to play college on a higher difficulty: Try to be a vocal male libertarian there. Write editorials for the paper that never get published. Sit through hours of mindless sensitivity training explaining all the speech limitations you must live with on campus. Learn how you can be charged with rape if your sex partner regrets the sex months later. Wonder every time you honestly answer a question in class from a libertarian point of view if you are killing any chance of getting a good grade in that course. Live every moment in a stew of intellectual opinion meant mainly to strip you of your individual liberties, while the self-same authoritarians weep and cry that your observation that minimum wage laws hurt low-skilled workers somehow is an aggression against them.

** OK, this is an exaggeration. I won't likely get shot. I don't want to understate how badly abused a lot of blacks and Hispanics are by the justice system. I would much rather be in front of the DOL than be a Mexican ziptied by Sheriff Joe. But it does give one the same feeling of helplessness, of inherent unfairness, of the unreasoning presumption of guilt and built-in bias.

First, let me establish a few background facts. Several years ago I headed an attempt to put a Constitutional amendment legalizing gay marriage on the ballot here in Arizona. As far back as 2004 I had a gay couple running a campground, and faced a customer petition demanding we remove them because they promoted moral degeneracy by being gay (it's for the children!). I told those customers to camp somewhere else, as we were not changing our staffing. Since then I have probably hired more gay couples to run campgrounds than anyone else in the business.

After a period of foreshadowing and rumor, the Equal Employment Opportunity Commission has now gone ahead and ruled that employment discrimination on the basis of sexual orientation is forbidden under existing federal civil rights law, specifically the current ban on sex discrimination. Congress may have declined to pass the long-pending Employment Non-Discrimination Act (ENDA), but no matter; the commission can reach the same result on its own just by reinterpreting current law.

There are multiple problems with non-discrimination law as currently implemented and enforced in the US. Larger companies, for example, struggle with disparate impact lawsuits from the EEOC, where statistical metrics that may have nothing to do with past discrimination are never-the-less used to justify discrimination penalties.

Smaller companies like mine tend to have a different problem. It is an unfortunate fact of life that the employees who do the worst job and/or break the rules the most frequently tend to be the same ones with the least self-awareness. As a result, no one wants to believe their termination is "fair", no matter how well documented or justified (I wrote yesterday that I have personally struggled with the same thing in my past employment).

Most folks grumble and walk away. But what if one is in a "protected group" under discrimination law? Now, not only is this person personally convinced that their firing was unfair, but there is a whole body of law geared to the assumption that their group may be treated unfairly. There are also many lawyers and activists who will tell them that they were almost certainly treated unfairly.

So a fair percentage of people in protected groups whom we fire for cause will file complaints with the government or outright sue us for discrimination. I will begin by saying that we have never lost a single one of these cases. In one or two we paid someone a nominal amount just to save legal costs of pursuing the case to the bitter end, but none of these cases were even close.

This easy ability to sue, enabled by our current implementation of discrimination law, imposes a couple of costs on us. First, each of these suits cost us about $20,000 to win (insurance companies are smart, they know exactly how this game works, and will not sell one an employment practices defense policy without at least a $25,000 deductible, particularly in California). It takes a lot of effort for the government, even if neutral and not biased against employers as they are in California, to determine if the employee who was fired happened to be Eskimo or if the employee was fired because he was an Eskimo. Unfortunately, the costs of this discovery are not symmetric. It costs employees and their attorneys virtually nothing to take a shot at us with such discrimination cases, but costs us$20,000 each to defend and win (talk about Pyrrhic victories). Which is why we sometimes will hand someone a few bucks even if their claim is absurd, just to avoid what turns out to be essentially legal blackmail.

Second, the threat of such suits and legal costs sometimes changes our behavior in ways that might be detrimental to our customers. A natural response to this kind of threat is to be double careful in documenting issues with employees in protected groups, meaning their termination for cause is often delayed. In a service business, almost anyone fired for cause has demonstrated characteristics that seriously hinder customer service, so drawing out the termination process also extends the negative impact on customers.

To make all this worse, many employees have discovered a legal dodge to enhance their post-employment lawsuits (I know that several advocacy groups in California recommend this tactic). If the employee suspects he or she is about to be fired, they will, before getting fired, claim all sorts of past discrimination. Now, when terminated, they can claim they where a whistle blower that that their termination was not for cause but really was retaliation against them for being a whistle-blower.

I remember one employee in California taking just this tactic, claiming discrimination just ahead of his termination, though he never presented any evidence beyond the vague claim. We wasted weeks with an outside investigator checking into his claims, all while customer complaints about the employee continued to come in. Eventually, we found nothing and fired him. And got sued. The case was so weak it was eventually dropped but it cost us -- you guessed it -- about $20,000 to defend. Given that this was more than the entire amount this operation had made over five years, it was the straw that broke the camel's back and led to us walking about from that particular operation and over half of our other California business.

Ellen Pao's supporters are blaming her departure from Reddit on sexism, despite the fact that the much of the opposition to her inside Reddit resulted from her termination of a popular female employee. I don't know what is inside her head of course, but after reading her piece in the WaPo, it sure doesn't look like she blames anything she did at Reddit for her failure there.

It is certainly possible to build a case that her decision-making at Reddit was ham-fisted and reactionary and not what the organization needed. I am the first to acknowledge that the dialog over large swaths of Reddit is toxic, but that is not a new thing. The odd bit to me is that Pao seems to have jumped right into the fray and immediately started swinging randomly. Why? What was the rush? I have never heard of a new leader jumping into an organization and immediately firing off culture-changing orders (there are a few exceptions to this, such as there-are-only -6-weeks-of-cash-in-the-bank crises, but this was not one of those). Even if you think you know what ails the company, you have to show the organization some respect and talk to a lot of people first. To me, it looked like a classic impatient arrogant technocrat's mistake -- but what does she think? Does she acknowledge error at all, even privately?

I say all this because I know quite personally what it is like to fail in business, and more importantly, just how very hard it is to acknowledge that such failure is one's own fault. To explain it, I have to give some background that will seem self-promoting.

I was always top in my class at school. I had my choice of Ivy League schools to attend, and graduated Princeton just a few hundredths of a GPA point (on the north side of 4) from being top of my department. Five years later, I did graduate first in my class at Harvard Business School. I write all this to say I entered the business world with supreme confidence.

The first signs of trouble were there in my very first job, though I only see them now. The engineering work at Exxon was easy, but I tended to drag my feet on tasks that required I seek out and pull together coalitions of experts. Ditto for my consulting work at McKinsey, where my analytical work and modelling were first-rate but my client building work was mediocre.

It was hard, really impossible at this point in my life, to accept I was failing at something. Even McKinsey's sending me to executive charm school (I kid you not, such things exist) was not a wake up call. I KNEW my analysis was awesome. I figured that was all that mattered. McKinsey was instead seeing an ADD guy with awkward people skills who would wander around the room eating off the side-board while in a formal meeting with a Fortune 25 CEO.

Things finally fell apart when I was working for a guy, really a legendary guy, named Chuck Knight at Emerson Electric. Again, I kept telling myself the analytical work I was doing was awesome, and I am sure it was. But even I couldn't fail to figure out that somehow my other people skills were totally wrong for corporate America.

And even then, when the organization made it abundantly clear I was not going to get any further promotions, pressing my face against the glass so to speak, I STILL could not fully face reality. I blamed my failings on a culture clash and similar things. You have heard this before -- "I left that company because it was totally screwed up." But it wasn't screwed up. It was a very solid, well-managed organization and a great place to work for the right people.

I was allowed to continue to avoid reality because I continued to fail upwards, getting an even larger job at a new company after Emerson based on my academic record and ability to do fabulous interviews (don't ask me why as an introvert I could do interviews but not one-on-one business discussions with my superiors, or why I thrive at speaking to large audiences but can't handle a cocktail party -- I don't know).

Again, at a large aerospace company, I had more great insights but little impact on the company. I created this awesome presentation -- it is still the best description of how profits are and are going to shift within the aerospace industry I have ever seen -- but I was being paid to do stuff that improved this year's sales and it wasn't happening (though to be a little fair to myself, making change in the aerospace business is a bit like trying to turn an aircraft carrier by pushing on the prow with a fishing boat).

It took me a couple more jobs and a taking a year off around the age of 40 to finally acknowledge all of this. After the pain of accepting failure, though, things really improved. I thought about what I did well and what I don't, and built my own company in large part based on those insights. Examples: Sales in my business are based more on creating huge, analytical written bid documents rather than face-to-face persuasion. Management is more about creating a great process and implementing that process consistently in scores of locations using technology and training. Most importantly, I am the boss, and many of my past interpersonal failures had to do with interacting with people with more authority, of which there are none in my company.

I don't deny that women or people of color in business likely face obstacles I have never faced, and I long for a world where that will no longer be true. But in trying to be sympathetic to women and people of various races and the discrimination they face, we also may be doing them a disservice, making it harder for them to gain self-awareness of their own abilities. After all, if I had been able to play the race or gender card as an excuse, I likely would never have gained what self-awareness I have today.

We have about 20 retail locations with credit card terminals. Typically, I have always bought the terminals because leasing is such a crazy bad deal. For example, Transfirst will lease you (via their partner First Data Global Leasing, or FDGL) a Hypercom 4220 for about $32 a month on a 48-month lease. That is about $1536 in payments total. Right now you can buy the same Hypercom 4220 invthis lease for about $179.

But despite this, I actually found myself talked into leasing a few of these Hypercom 4220 terminals. I was told by Transfirst (the merchant company) that a technology transformation was coming (this was true) and that the advantage of leasing was that if the terminals become obsolete, they will be upgraded automatically (this turned out to be a lie).

Note that this was stupid, stupid, stupid on my part. I admit it. I could have still bought them and have been better off after 6 months, even if it became obsolete, than leasing. Mea culpa. My only excuse is that I had developed a lot of trust in my old processor Solveras and didn't realize how much their customer service would change for the worse when they got bought by Transfirst.

However, the really irritating part occurred when I got an email from Transfirst saying that my Hypercom 4220's would essentially be obsolete after October, 2015 because these terminals can't handle the new chip cards (technically I could still use them, but at a serious liability risk, which is not acceptable). So I called Transfirst and asked them what was going to happen on my equipment they leased me that they now have told me is obsolete. They said that I could upgrade the Hypercom's on my lease to Ingenico ICT220's for a $189 fee.

Well, it turns out that Ingenico ICT220's retail for about $160. So here was the upgrade option they offered on my lease -- I could pay more than the retail price of a new terminal in order to substitute that new terminal on my account, and having just paid for the terminal, the terminal then would become property of the leasing company and must be returned at the end of the lease, which all the while is still charging me $32 a month.

I called my sales agent, the customer support staff, the equipment transition team -- they all said the same thing. I could not believe it. The deal was so bad that even one of their competitors, whom I had started talking to, urged me to check with Transfirst more carefully because they could not believe Transfirst were offering such an awful arrangement. But they were.

So I am switching merchant companies and buying all new terminals. I will return to Transfirst all their equipment and pay off the remaining months on the lease. It is not often that a vendor of mine is so bad that I pay substantial money to get away from them, but getting away from Transfirst justified the cost.

By the way, for merchant companies reading this, please do not add yourself, based on this post, to the 3-4 calls a day I get trying to sell me credit card processing. I have a good deal for half my business with Bank of American, have always been happy with their service, and am moving my Transfirst business to them.

Postscript: One piece of advice on choosing a merchant account. When I ask for quotes on merchant services, I ask now that the bid be quoted as a spread. Basically MC/Visa have a set of rates they charge, sort of wholesale rates everyone must pay. There are zillions of rates for various types of cards (for example those rewards cards you love can pay you because they get a higher fee from merchants for the same transaction). If you just get a rate quote, you will get zillions of rates and it will be almost impossible to compare against another quote, particularly if you don't know your typical mix of card types. If you ask for a spread, e.g. 10 basis points over wholesale on all cards, you know exactly what you are getting and that there are not any bad deals buried in that rate list. It is also really easy to compare to other quotes.

The other advantage of this is that when MC/Visa change their rates (always up) your rates just go up by the amount of the rate increase. Without a spread deal, merchant processors can take advantage of MC/Visa rate changes to slip in a few more basis points for themselves. How would you ever know?

Bloomberg (via Zero Hedge) had this chart on Disney theme park entrance prices:

A few random thoughts:

This highlights how hard it is to do inflation statistics correctly. For example, the ticket being sold in 1971 is completely different from the one being sold in 2015. The 2015 ticket gets one access without additional charge to all the attractions. The 1971 ticket required purchase of additional ride tickets (the famous, among Disney fans, A-E tickets). So this is not an apples to apples comparison. Further, Disney has huge discounts for multi-day tickets. The first day may cost $105, but adding a fourth day to a three day ticket costs just a trivial few bucks. Local residents who come often for a single day get special rates as well. So the inflation rate here grossly overestimates that actual increase in per person, per trip total spending for access to park attractions

This is a great case in pricing strategy. Around 1980, the Bass family bought into a large ownership percentage of Disney. The story I am about to tell is often credited to their influence, but I am not positive. Never-the-less, someone had a big "aha!" moment at Disney. They realized that families were taking trips just to visit DisneyWorld. These trips cost hundreds, even thousands of dollars. The families were thus paying hundreds of dollars per person to enjoy Disney, of which Disney was reaping... $9.50 a day. They had a stupendously valuable product (as far as consumers were concerned) but everyone else in the supply chain was grabbing most of the value they created. So Disney raised prices, on the theory that if a family were paying over a thousand dollars to get and stay there, they would not object to paying an extra $50 at the gate. And they were right.

The article begins by relating that VFX and digital effects specialty houses all lose money, even when they are providing effects for wildly profitable movies (e.g. Avengers) and purports to explain why this should be. The author believes that this is a result of Hollywood purposely criticizing the artistry of VFX movies as a way to keep returns in the VFX companies down (and thus increase the returns of film producers).

As the debate surrounding what visual effects are worth rages on, it is clear that the studios themselves have an interest in perpetuating the myth that VFX are the product of clinical assembly lines and the results are equally lifeless and mechanical. Blaming computers for the dumbing down of movies has become a journalistic trope that is bandied about to squeeze the one part of the Hollywood machine that has no union or organizational skill to push back. The right hand asserts they are something not worth paying top dollar for, while the left lines up an interminable roster of VFX-based box office juggernauts for the foreseeable future.

The author goes so far as to say that Avatar was denied the best picture Oscar specifically to support the anti-VFX sentiment and keep returns of VFX companies down (emphasis added).

In 2010, James Cameron’s Avatar became the highest grossing film of all time just 41 days after its release, raking in an incredible $2.7 billion by the end of its run. Weta Digital, the VFX studio that created the majority of the visual effects, along with Lightstorm Entertainment, invested years in developing the tools and talent necessary to create Cameron’s almost entirely computer generated vision, with the cost of making the film rumored to be upwards of $500 million. Cameron had promised to show the world what visual effects could do and he succeeded. The results were universally lauded as visually stunning and unparalleled.

Yet, rather famously, the film and Cameron were snubbed that year at the Academy Awards, both for Best Picture and Best Director. The blame was laid at the feet of the critical success of The Hurt Locker. However, awarding Avatar the Academy’s highest honor would have been acknowledging visual effects as not only lucrative, but high art as well, worthy of its astronomical price tag. And that was a bargaining chip Hollywood was unwilling to concede to an industry it continues to hold hostage with threats of outsourcing to unskilled laborers around the globe.

This hypothesis seems outlandish, and in fact the author never really provides any evidence whatsoever for her hypothesis. At least equally likely is that Hollywood insiders are snobbish and conservative and reject new approaches to film-making in a way that the public does not. Or it could be that Avatar wasn't a very good movie (go try to watch it again today, you will be surprised what a yawner it is). So why are VFX companies really losing money on profitable films? Let's take a step back, because there is a useful business lesson buried in here somewhere. I think.

This discussion is a sub-set of an age-old business problem -- how do rents in a supply chain get divided up? Think of the billion plus dollars the new Avengers movie will make. Everyone in the supply chain for making that movie, from the actors to the caterers to the VFX houses to the distribution companies believe their contribution has immense value, and that they should be getting a solid cut of the profits. But profits in a supply chain are not divided up based on some third party assessing value, they are divided up by negotiation. And the results of that negotiation depend on a lot of factors -- the number of competitors, the uniqueness of the service, regulatory rules, etc. The most visible example of this sort of negotiation we see frequently in the news is in sports, where players and team owners are explicitly negotiating the division of the end revenue pie between themselves.

If we return to the article, the author actually gives us a hint of the true dynamic that is likely bringing down VFX profits.

The international subsidies-driven business model under which VFX companies operate has been well documented.In pursuit of tax rebates offered by various governments to produce films in their jurisdiction, studios insist that VFX companies open branches in these locations or reduce their bids by the amount of the subsidy in question. Even as studios, directors, and audiences demand the latest in cutting edge technology, VFX houses must underbid one another to get the work and many have been shuttered due to operational losses in the wake of explosive blockbuster budgets. The cost of research and development, shrinking schedules, and the unlimited changes that are the building blocks of every tentpole film, are shouldered entirely by VFX houses.

This is the best clue we get to the real problem. Here is what I infer from this paragraph:

This is a high fixed cost industry. There are enormous up-front investments in research into new techniques and large investments in the latest technology, which presumably must be constantly refreshed because it has a short half-life before it is out of date. The situation is worsened by government policy, which provides incentives for VFX companies to build extra capacity in multiple countries, losing economy of scale benefits from large concentrated production facilities. One would presume from this that these companies' marginal cost of output, say 15 seconds of finished effects, is way way below their total costs.

There is rivalry among VFX companies that seem to have excess capacity, such that bidding for work is very aggressive. In such situations (think American railroads in the late 19th century) competitors lower prices down to marginal cost to keep their capacity and their trained people working. Over time, of course, this leads to numerous bankruptices

I will add a third point which the author fails to cover. To do so I will return to one of my favorite things I learned at Harvard Business School (HBS). At HBS, in the first two days of strategy class, we studied two very different business cases. The first was of a water meter manufacturer, a dead boring predictable unsexy business. The second was a semiconductor company, which was hip and cool and really sexy. It turned out that the water meter company coined money. The semiconductor business was in and out of bankruptcy.

Why? Well the water meter company had limited investment (made the same meters the same way for decades) and made most of its money off the replacement market, where it had no competitors since users pretty much had to replace with the same meter. The semiconductor business had numerous shifting competitors and was constantly trying to scrape up enough investment money to keep up with shifting technology. But there was one more difference. By being sexy, tons of people wanted to be in the semiconductor business. They got non-monetary benefits from being in it (ie it was cool and interesting). When there is an industry where lots of people are getting into the business for reasons other than making money, look out! The profits are probably going to be terrible. This is why most restaurants fail. The business-for-sale listings are awash in brew pubs. The aviation industry was like this for years, and I would argue this also suppresses rents in farming.

I don't know this for a fact, but I would bet that the VFX industry attracts a lot of people because it is sexy. Yes, like a lot of programming, the actual work is detailed and dull. But if the coding is detailed and dull, would you rather be doing it for Exxon's new back-office system or to put Ironman on the big screen (and have your name deep into the film credits, seen by the dozen or so people who hang around waiting for the Marvel Easter egg at the end)?

This is why I think a conspiracy theory to believe Hollywood is dissing the artistry of VFX movies as a way to keep VFX company rents down is silly. It is totally unnecessary to explain the bad rents. Had you told me it was a high investment business with huge fixed costs and much lower marginal costs and alot of rivalry driven by participants who piled into the business because it was sexy, I would have told you to stop right there and I could have immediately predicted poor returns and bankruptcies.

So what can VFX companies do? I have no idea. The first idea I would offer them is branding. If you are buried deep in the supply chain and want to increase your bargaining power, one way to do it is to develop a brand with the end consumer. If consumers suddenly latch on to, say, the CoyoteFX brand as being innovative or better in some way, such that they might be more likely to go to a movie with CoyoteFX sequences, then CoyoteFX now has a LOT more power in negotiations with producers. Dolby Sound is a great example -- you probably don't even know what it is but movies used to advertise they had it. Certain camera technologies like Panavision are another, where movies actually sold themselves in part on the features of one member of their supply chain. As a digital house, Pixar effectively did this -- so well in fact its brand actually was bigger than Disney's (its distributor) for a while, and Disney was forced to buy them. This does not happen just in movies. I just bought a car that advertised it had a premium Bose sound system. The car maker doesn't advertise who made, say, the fuel tanks, so my guess is that Bose, via branding, gets a better cut of the supply chain than does the fuel tank maker.

I am going to oversimplify, but the essence of bank risk is that they borrow short-term and invest/lend long-term. This is a money-making strategy in that one can often borrow short-term much cheaper than one can borrow long term. This spread between long and short term rates is due to people valuing liquidity. You probably have experienced it yourself when buying a certificate of deposit (CD). The rates for 5 or 10 year CD's are higher, but do you really want to tie your money up for so long? What if rates improve and you find yourself locked into a CD with lower rates? What if you need the money for an emergency? Your concern for having your money locked up is what a preference for liquidity means.

So banks live off this spread. But there are risks, just like you understood there are risks to locking your money in a long-term CD. Imagine the bank is lending for mortgages and AAA corporate customers at 6%. To fund that, they have some shareholder money, which is a long-term investment. But they make the rest up with things like deposits and commercial paper (essentially 90-day or shorter notes). We will leave the Fed out for this. There are two main risks

Short term interest rates rise, such that the spread between their short term borrowing and long-term investments narrows, or even reverses to negative

Worse, the short term money can just disappear. In panics, as we saw in the last financial crisis, the commercial paper market essentially dries up and depositors withdraw their money at the first sign of trouble (this is mitigated for small depositors by deposit insurance but not for large depositors who are not 100% covered).

These risks are made worse when banks or bank-like institutions try to improve the spread they are earning by making riskier investments, thus increasing the spread between their borrowing and investing, but also increasing risk. This is particularly so because these risky investments tend to go south at the same time that short-term credit markets dry up. In fact, the two are closely related.

GE’s news release announcing its latest and greatest reduction of GE Capital summed up the move beautifully, saying “the business model for large wholesale-funded financial companies has changed, making it increasingly difficult to generate acceptable returns going forward.â€

“Wholesale-funded†refers to GE Capital’s traditional reliance on the commercial paper market for liquidity. The problem with this short-term funding model for a balance sheet with long-term assets is that during a financial crisis, overnight liquidity tends to dry up as it did for GE late in 2008. When the company had difficulty finding buyers for its paper, the Federal Deposit Insurance Corp. stepped in and through its Temporary Liquidity Guarantee Program (TLGP) was covering $21.8 billion of GE commercial paper. GE Capital registered for up to $126 billion in commercial-paper guarantees under the TLGP.

If you have a AAA credit rating, you can always, always make money in the good times borrowing short and investing long. You can make even more money borrowing short and investing long and risky. GE made their money in the good times, and then when the model absolutely inevitably fell on its face in the bad times, we taxpayers bailed them out.

Which leads me to think back to Enron. Enron is associated in most people's minds with fraud, and Enron played a lot of funky accounting games to disguise its true financial position from its owners. But at the end of the day, that fraud was not why it failed. Enron failed because it was essentially a bank that was borrowing short and investing long. When the liquidity crisis arrived and they couldn't borrow short any more, they went bankrupt. Jeff Skilling didn't actually go to jail for accounting fraud, he went to jail for making potentially inaccurate positive statements to shareholders to try to head off the crisis of confidence (and the resulting liquidity crisis). Something every CEO in history has done in a liquidity crisis (back in 2008 I wrote an article comparing Bear Stearns crash and the actions of its CEO to Enron's; two days later the Economist went into great depth on the same topic).

So the difference between GE and Enron? The government bailed out GE by guaranteeing its commercial paper (thus solving its problem of access to short term funding) and did nothing for Enron. Obviously the time and place and government officials involved differed, but I would also offer up two differences:

Few really understood what mad genius Jeff Skilling was doing at Enron (I can call him that because I actually worked with him briefly at McKinsey, which you can also take as a disclosure). With Enron so opaque to outsiders, for which a lot of the blame has to be put on Enron managers for making it that way, it was far easier to ascribe its problems to fraud rather than the liquidity crisis that was well-understood at Bear or Lehman or GE.

Enron failed to convince the world it posed systematic risk, which in hindsight it did not. GE and other big banks survived 2008 and got bailed out because they convinced the government they would take everyone down with them. They followed the strategy of the Joker in The Dark Knight, who revealed to a hostile room a coat full of grenades with this finger ready to pull the pins if they didn't let him out alive.

Artist's rendering of 2008 business strategy of GE Capital, Citicorp, Bank of America, Goldman Sachs, GMAC, etc.

Postscript: For those not clicking through, I though this bit from the 2008 Economist article was pretty thought-provoking:

For many people, the mere fact of Enron's collapse is evidence that Mr Skilling and his old mentor and boss, Ken Lay, who died between hisconviction and sentencing, presided over a fraudulent house of cards. Yet Mr Skilling has always argued that Enron's collapse largely resulted from a loss of trust in the firm by its financial-market counterparties, who engaged in the equivalent of a bank run. Certainly, the amounts of money involved in the specific frauds identified at Enron were small compared to the amount of shareholder value that was ultimately destroyed when it plunged into bankruptcy.

Yet recent events in the financial markets add some weight to Mr Skilling's story"â€though nobody is (yet) alleging the sort of fraudulentbehaviour on Wall Street that apparently took place at Enron. The hastily arranged purchase of Bear Stearns by JP Morgan Chase is the result of exactly such a bank run on the bank, as Bear's counterparties lost faith in it. This has seen the destruction of most of its roughly $20-billion market capitalisation since January 2007. By comparison, $65 billion was wiped out at Enron, and $190 billion at Citigroup since May 2007, as the credit crunch turned into a crisis in capitalism.

Mr Skilling's defence team unearthed another apparent inconsistency in Mr Fastow's testimony that resonates with today's events. As Enronentered its death spiral, Mr Lay held a meeting to reassure employees that the firm was still in good shape, and that its "liquidity was strong". The composite suggested that Mr Fastow "felt [Mr Lay's comment] was an overstatement" stemming from Mr Lay's need to "increase public confidence" in the firm.

The original FBI notes say that Mr Fastow thought the comment "fair". The jury found Mr Lay guilty of fraud at least partly because it believed the government's allegations that Mr Lay knew such bullish statements were false when he made them.

As recently as March 12th, Alan Schwartz, the chief executive of Bear Stearns, issued a statement responding to rumours that it was introuble, saying that "we don't see any pressure on our liquidity, let alone a liquidity crisis." Two days later, only an emergency credit line arranged by the Federal Reserve was keeping the investment bank alive. (Meanwhile, as its share price tumbled on rumours of trouble onMarch 17th, Lehman Brothers issued a statement confirming that its "liquidity is very strong.")

Although it can do nothing for Mr Lay, the fate of Bear Stearns illustrates how fast quickly a firm's prospects can go from promising to non-existent when counterparties lose confidence in it. The rapid loss of market value so soon after a bullish comment from a chief executive may, judging by one reading of Enron's experience, get prosecutorial juices going, should the financial crisis get so bad that the public demands locking up some prominent Wall Streeters.

Our securities laws are written to protect shareholders and rightly take a dim view of CEO's make false statements about the condition of a company. But if you owned stock in a company facing such a crisis, what would you want your CEO saying? "Everything is fine, nothing to see here" or "We're toast, call Blackstone to pick up the carcass"?

My absolute favorite example of corporations using social causes as cover for cost-cutting is in hotels. You have probably seen it -- the little cards in the bathroom that say that you can help save the world by reusing your towels. This is freaking brilliant marketing. It looks all environmental and stuff, but in fact they are just asking your permission to save money by not doing laundry.

Men negotiate harder than women do and sometimes women get penalized when they do negotiate,’ she said. ‘So as part of our recruiting process we don’t negotiate with candidates. We come up with an offer that we think is fair. If you want more equity, we’ll let you swap a little bit of your cash salary for equity, but we aren’t going to reward people who are better negotiators with more compensation.’

Like the towels in hotels are not washed to save the world, this is marketed as fairness to women, but note in fact that women don't actually get anything. What the company gets is an excuse to make their salaries take-it-or-leave-it offers and helps the company draw the line against expensive negotiation that might increase their payroll costs.

Postscript: Yes, I understand the theory of negotiation and price discrimination, as used by auto dealers. One can make an argument that setting prices high (or wages low) and then allowing negotiation by the most wage or price sensitive is the best way to optimize profits, and that Pao's plan in the long-term may actually raise their total compensation costs for the same quality people. I don't think she is thinking that far ahead.

Update 2/1/2016: I will not comment further at the moment on Applied Underwriters as they are currently suing me to have this article below removed. So you will need to look elsewhere for news on AU, of which there appears to be plenty. For example, here and here. The State of California Insurance Commission, via an Administrative Law Judge's decision, has ruled on the legality of the AU product discussed below. That ruling (pdf) can be downloaded here. I would love to comment on it but I will have to leave the evaluation to you. If you can't read the whole thing pages 33 and 34 are worth your time, as well as the conclusions that begin on page 59.

Well, I have managed to get myself into a scam. It is not your normal scam, like the ones that are run by some mafia boiler room with guys working under aliases. This scam comes via a major insurance company called Applied Underwriters (working under the names California Insurance Company and Continental Indemnity Company) which is owned by Berkshire Hathaway and none other than Warren Buffett. If you feel sorry for Warren Buffett and want to give him a large interest-free loan for an indeterminate number of years, this is your program.

Update 4/16: Let me insert here that Applied Underwriters has sent me a letter threatening a libel suit if I do not take down this post and a parallel review at Yelp. AU Takedown demand here (pdf). The gist of the matter seems to be the word "scam". By the text of their letter, they seem to believe that "scam" is libelous because their company is well-rated financially and that they provide reasonable claims service. I concede both these facts. However, I called it a "scam" because there is a big undisclosed cost to their product that was never mentioned in the sales process, and that could only be recognized by its omission in the contract I signed -- that there is nothing in the contract committing them to any time-frame under which to return deposits and excess premiums I have paid, which may well amount to hundreds of thousands of dollars. This fact about the contract is confirmed by their customer service staff, who have said further that the typical time-frame to return such over-collections and deposits is 3-7 years after the contract ends, or at least 6-10 years after the first of the deposits was made.

So is this a "scam"? I believe that this issue is costly enough, and hard enough to detect, and far enough outside of expected business practices to be called such. You may have your own opinion, but ask yourself -- When you enter into, say, a lease and have to put down a security deposit, is it your reasonable expectation that the landlord has the right in your lease to keep your deposit for 3-7 years (or more) after you move out? /Update

Anyway, let's take a step back and look at this in detail.

First, I need to give a bit of background on how workers comp works. When you are a new company, they assign you an experience rating -- that is a multiplier of your premium based on past loss experience. There is some default starting number that if I remember right, in most states, is a bit over 1.0x. Each year, the workers comp world looks back at your past history and computes a new loss rating -- higher if you have had more payouts, lower if not. Generally it is based on three years experience not counting the last year (so 2-4 years in the past). Your future premiums get multiplied by this loss rating.

Several years ago we had a couple bad injuries that drove our loss number into the 1.7-1.9x area. Neither were really due to a bad safety issue, but both involved workers in their seventies where a minor initial injury led to all sorts of complications. Anyway, my agent at the time calls me one day a couple of weeks before renewal and says that none of the major companies will renew me. This seemed odd to me -- I understood that my recent claims history was not good, but isn't that what the premium multiplier was for? In fact, if my loss history returned to normal, they would make a fortune as I paid high rates based on old losses but had fewer new ones.

Apparently, though, insurance companies have fixed rules that keep them from underwriting higher loss ratings. Probably for the same reason Vegas won't take action on Ivy League football games any more -- just too much variability. I found out later with my new broker we could probably have overcome this, but I learned that too late.

My broker at the time put me into a 3-year program from Applied Underwriters, in part because they were taking everybody. This program was set up differently from most workers comp programs. You had a basic policy, but there was a second (almost indecipherable to laymen) reinsurance agreement that adjusted the rates of the basic policy based on you actual claims. Here is the agreement (pdf) In other words, based on your claims, they would figure up at the end how much you owed and what your premium multiplier would be.

I saw two red flags that I ignored in signing up. 1) The reinsurance agreement was impossible to understand, violating one of my foundational rules that I shouldn't sign things I don't understand. And 2) The rate structure was very suspicious. They touted a rate structure that could go as low as, say, $100,000 a year and was capped around $400,000 a year. But when you pulled out a calculator, the $100,000 was virtually unobtainable. It would require about zero claims. If there were any claims at all, even for a few bandaids, the price would march up to $400,000 really fast. It was the equivalent of a credit card teaser rate, and it should have made me suspicious.

Anyway, I was desperate. For a business like mine, being told I had no workers comp insurance just a few weeks before the old policy ran out was a death sentence. No one would write me or even quote me a policy that fast. So I took the Applied Underwriters offer. Shame on me, I should have worked on this much harder.

I won't bore you further with my voyage of discovery in trying to figure out how this thing works. I will just tell you the results that I have found. There are apparently other companies with similar issues, one of which is documented here: Applied Underwriter Suit (pdf)Newsletter publisher objected to scan of article, so I have taken it down at their request. Here is a link to roughly the same article.

I spent hours and hours trying to figure out AU's statements. There is a whole set of terminology to learn that is actually not used in most of the rest of the workers comp world. The key page of the statement is page 7, which I will show below because it highlights several of the issues with Applied. Page 7 is the page where the monthly premium is "calculated". I have added the red numbers and arrows for the discussion below.

Here are some of the Applied Underwriter problems:

Large deposits that must be made each year and may never be returned. You can see that I am making deposits over $40,000 a year. And that is each year. The first year deposit is not returned. The second year and third year are just added to it. And I have found out since I joined this program that they are not contractually obligated to return them in any time frame. Maybe some guy who was hurt in his thirties has a relapse and claims more money when he is 75. Gotta keep your deposit just in case, don't we? The timing of the return of your deposits (and overpaid premiums below) is entirely at their discretion, and that has been confirmed by their customer service staff. In fact, their standard answer is that on average, such monies are not returned to customers for 3-7 years after the contract ends, or at least 6-10 years after the first deposits were made.

Premiums based on the worst of your experience and their estimate of your losses, and they keep the difference for years and years. For those in the same trap as me, I will try to explain the numbers above. The estimated loss pick containment at the top is basically their estimate of your losses. Note that it drives every number on the page and is basically their arbitrary number -- they could have set it anywhere. The loss pick containment to date is just pro rated for the amount of the year that has gone by. The 65% is an arbitrary number. The $25,278 is my actual losses to date. You can see where I point with #2 above, though, that my losses are irrelevant to my premiums. They take the higher of my losses and what is essentially their estimate of my losses and I pay based on that. Note that their higher number is not based on the reserved amounts on actual claims -- the $25,278 includes their reserves. It is just the number they established at the beginning of my policy they think my claims are going to be and gosh darnit they are going to stick to that (and my claims even in my worst year in history were never even half of their estimate). Yes, at the end of the policy if my losses stay low, they owe me money back for all the premium they overcharged me based on their arbitrarily high estimates. But see #1 above -- there is no time horizon under which they have to return the money. They can keep it for years and years.

The final premium is, after all these calculations, entirely arbitrary. So after this loss calculation (which essentially just defaults to their arbitrarily high estimate and not my actual loss history) they do some premium calculations. These actually sort of make sense if you stare at the agreements for a really long time. But then we get to the line I point to in red labelled 3. It is the actual amount I owe. But it does not foot to any other number on the page. How do they come up with this? They won't say. To anyone. It might as well be arbitrary. I actually had some dead time and took all my reports and tried to regress to a formula they use for this, but I couldn't figure it out. So all the calculation on this page is just a sham, it's the mechanical wizard in the Wizard of Oz. It looks good, but does not actually directly lead to what you are billed.

So I thought I understood my problems. I put in large deposits and overpaid premiums based on arbitrarily high loss estimates they make -- all of which will take me years and years of effort to maybe get back. It turns out that I likely will have a third problem. In the lawsuit linked above, the plaintiff complains that when they left the program after three years, Applied arbitrarily wrote up all their estimated losses on open claims to stratospheric levels and then demanded a large final premium payment at the end. Folks on Yelp complain of the same thing. You should know how this works by now -- the plaintiff will theoretically get all this back someday, maybe, when the claims prove to be less costly, but in the mean time Warren Buffet gets to invest the money for years and years (cost of capital = 0) until it is returned.

This is why I think Applied Underwriters actually likes companies with high lost histories. Rather than costs, losses for them are excuses to over-collect on deposits and premiums -- money that can then be invested and held for years free of charge.

As an aside, I want to thank my new agents at Interwest Insurance for helping decipher all of this. They actually flew a guy in to help me understand this policy. They didn't get me into it, but they are helping me pick up the pieces as best we can.

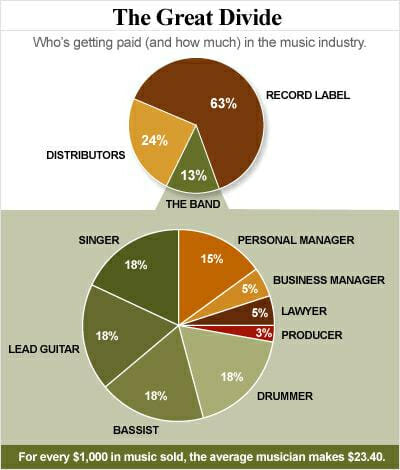

We have all heard that artists make very little money from their songs, and get "ripped off"by record labels and other folks in the chain. I have always had mixed reactions to this. I have no doubt that, with zero power and a burning desire to "make it big", young acts sign uneven deals with record labels. However, I find it hard to believe that Beyonce is getting hosed in that negotiation.

I saw this chart in TechDirt about where the money consumers spend on music goes (I think this is for a CD sale):

So the performers themselves get about 9% of the retail price after everyone in the chain is paid. That certainly seems paltry -- after all, they are the owners and creators of the music. Everyone else is just in the service chain to make sure the music reaches the customers, all the accounting is done, the legal documents are correct, etc.

But it turns out that they may not be doing that badly. I am a shareholder of ExxonMobil (XOM). I own a piece of all the oil that XOM owns and controls, along with all the other shareholders. Think of us as the band, though a really big band with lots of players. That oil we own, like the band's music, has a ton of value. When sold as raw crude, it goes for $40-$60 a barrel nowadays. When sold in pieces (such as gasoline, or asphalt, or lubrication oil) it can sell for hundreds of dollars a barrel.

But out of those proceeds, we have to pay people to help us. We have to pay managers, and lawyers. We have to pay oilfield services companies and equipment companies and transportation companies. We have to pay retailers. When all those payments are made, before taxes, in 2014 we were left with just under 8% of every dollar we sell. We own all this oil and we are not even getting as much as a musician!

Does that mean that Exxon shareholders are getting "ripped off" by Haliburton and Burlington Northern? Is Wal-Mart getting ripped off by Proctor and Gamble? Is Humana getting ripped off by GE imaging? No?

I will reveal the ugly secret: There is one person who is "ripping off" all of these folks, from Exxon to Rihanna to me. That person is.... the consumer. Yep, there are certainly many examples of people signing bad contracts in all these businesses, but the only entity systematically and consistently ripping all these folks off is us. Because in a capitalist economy, we have the ultimate power. We drive down the street to get the gas that is 10 cents cheaper, we now shop for our books and TVs at Wal-Mart and Amazon rather than at Borders and Best Buy, and we buy 99-cent individual songs on iTunes instead of buying a whole CD of songs we don't want for $14.99.

A while back I (for a short time) chaired an effort to get a ballot initiative in Arizona to change to Constitution to allow gay marriage. In the process, gay rights advocates approached me for support of another law to add LGBT persons to the list of protected classes that are covered by workplace discrimination laws.

I refused to help, and these folks immediately labeled me a hypocrite. To be fair to them, they honestly thought that workplace discrimination laws did exactly what they intended to do - ban workplace discrimination of an overt sort (e.g., "what, you're gay? Well, you can't work around here any more"). But anti-discrimination law has a lot of other unintended consequences that are all bad for even the most fair-minded business owner.

Because most of the actual stories I have been through are (and should be) confidential, I will illustrate the problem from a story out of the national news.

Debbie Wasserman Schultz is Chair of the Democratic Party. Several years ago various party members became dissatisfied with her leadership, a pretty normal occurrence for such a position, particularly after Congressional losses in several elections. I compare the job to that of an NFL coach, who has job security only as long as he is winning (see: Jim Harbaugh in San Francisco).

Wasserman Schultz’s position as the head of the DNC has long been a source of contention among Democrats, and Politico has previously documented the issue. In September 2014, Wasserman Schultz’s gaffes caught up to her when a string of Democrats voiced their distaste for the way the Florida congresswoman had led the party.

That report found tension between Wasserman Schultz and Obama dating back to 2011 .... At the time, Wasserman Schultz had allegedly complained to Obama about not being able to hire a donor’s daughter to work for her at the DNC.

“Obama summed up his reaction to staff afterward: ‘Really?’ ” according to a source that was present.

So maybe Obama didn’t like Wasserman Schultz’s brashness or her propensity to spout gaffeafter gaffe.

So, faced with threats of losing her position based on poor job performance, her response was this:

Democratic National Committee Chairwoman Debbie Wasserman Schultz was prepared to go full force against President Obama if he tried to replace her in 2013.

Wasserman Schultz, according to Politico, was going to accuse Obama of being anti-woman and anti-Semitic — apparently to cover all the bases — if he dared consider replacing her as chairwoman.

There is absolutely no rational reason to believe President Obama wanted to fire her because she was a woman. Seriously, Valerie Jarrett practically runs the country but Obama doesn't like Shultz because she is a woman? I would bet that in fact she was hired for the position in large part because she was a woman. But she was perfectly willing to use the fact that she happened to be in some protected employment classes to try to head off a merit-based firing.

For businesses, this means two things

It typically takes much longer to terminate someone in a protected class, because businesses want to make sure they have an absolutely iron-clad case if the termination is later challenged. For a service business like ours, this sometimes means tolerating dangerous behavior or really bad customer service longer (with all the risks that entails) from someone in a protected group rather than from, say, a white male.

A large number of employees in protected groups will file grievances to the state, or even sue, over even the most well-documented and justified termination. Even when employers win such cases, each one take tens of thousands of dollars in legal fees to win. As interpreted by courts and state civil rights agencies, anti-discrimination law seems to create burden of proof on the part of employers to prove they did nothing wrong, rather than the other way around.

CBE is closing its open outcry pits (e.g. the type of trading portrayed in the movie Trading Places). Time to short the manufacturers of brightly covered jackets (from my very very limited experience observing the pit in Chicago, one unreality of Trading Places is that the traders are all wearing fairly normal business attire).

I wish we saw this attitude more often, particularly among large corporations (from an article discussing aftermarket ticket prices for the Super Bowl).

"This is really something we never anticipated," said Will Flaherty, director of growth at SeatGeek. "The cheapest seat on SeatGeek right now is $8,000, but no site seems to have any inventory." Flaherty believes speculative buying is behind the spike. Ticket brokers frequently sell "air" to their customers, taking orders before they have tickets in hand. "We've noticed significantly more speculative selling activity than in recent years," Flaherty said. "Over the last few days, those sellers have been scrambling to buy up tickets to fill their orders, resulting in the Super Bowl ticket version of a short squeeze. Brokers with tickets in hand have been taking advantage of their leverage, raising prices dramatically and arbitrarily withholding some of their inventory."

Ety Rybak, co-founder of the high-end brokerage Inside Sports & Entertainment Group, has spent more than anticipated this time around to fulfill orders before the game. "I can tell you some ugly horror stories about what I have had to pay. But that’s part of the business," he said. "If I sold you tickets for $2,500, and I have to pay $7,500 to do it, unfortunately that’s the world that I chose to live in." The flip side to the high costs is a brisk business in late orders.

Maybe the US sugar cartel, among many other groups, could discover this approach to individual responsibility.

The Left spends a lot of time railing against the rich and large corporations. But in practice, they seem hell-bent on lining the pockets of exactly these groups. Today the ECB announces a one trillion plus euro government buyback of public and private securities.

Between Japan, the US, and now Europe, the world's central banks are printing money like crazy to inflate securities values around the world -- debt securities directly by buying them but indirectly a lot of the money spills over into stocks as well. This has been a huge windfall for people whose income mostly comes from capital gains (i.e. rich people) and institutions that have access to bond and equity markets (i.e. large corporations). You can see the effects in the skyrocketing income inequality numbers over the last 6 years. On the other end, as a small business person, you sure can't see any difference in my access or cost of capital. It is still just as impossible to get a cash flow loan as it always was.

This is so common that there ought to be a name for it (perhaps there is and I just don't know it): Writer does a story or study on some trend, in this case the downfall of the enclosed shopping mall. In each case, the writer discovers that such malls died because of ... all the things the writer already holds dear. If the writer hates American consumerism, then the fall of such malls is a backlash against American consumerism.

It is interesting to note that all of the ideas quoted are demand-side explanations, e.g. why might consumers stop going to large enclosed malls. And certainly I find the newer outdoor malls more congenial personally, but this can't be the only explanation. Here in north Phoenix, I can see the dying enclosed Paradise Valley Mall out my window, but just a few miles away is the Scottsdale Fashion Square, a traditional mall that appears to be going great guns. Ditto the Galleria in Houston. Perhaps part of the answer is that enclosed malls were simply overbuilt and that people are willing to drive a bit to get to the best enclosed mall in town rather than a smaller version closer to their home (certainly Mall of America made a big bet on that effect).

But it also strikes me there are supply side considerations. The mall out my window is a huge waste of space, surrounded by parking lots the size of a small county. And it's just retail. Modern outdoor malls allow developers to mix shopping, living, and office space in what looks to my eye to be a much denser development. All these malls have stores on the ground floor with condos and offices up above. To my not-real-estate-trained eye, this would seem to increase the potential rents in a given piece of land and provide some synergies among the local businesses (e.g. office workers and residents eat and shop in the mall shops). In some sense it is a re-imagining of the downtown urban space in a suburban context. This is ironic because it is something urban planners have been trying to force for decades and here comes the free market to do it on its own.

People also like going to newer facilities. Just ask hotel owners. If owners do not totally refresh a hotel every 20 years or so, people stop visiting and rates fall. The same is true of gas stations and convenience stores. When I worked at Exxon briefly, they said they budgeted to totally rebuild a gas station every 20 years. So it is not impossible there is a big supply-side explanation here -- if people are reluctant to go to establishments over 20 years old, then visitation of enclosed malls should be collapsing right about now, 20 years after they stopped being built. A shift in developer preferences could be a large element driving this behavior. I don't insist that the supply side and real estate incentives are the only explanation, but I think they are a part of it.

Edelman soon came to the horrifying realization that he had been overcharged. By a total of $4.

If you’ve ever wondered what happens when a Harvard Business School professor thinks a family-run Chinese restaurant screwed him out of $4, you’re about to find out.

(Hint: It involves invocation of the Massachusetts Consumer Protection Statute and multiple threats of legal action.)

Here was the letter I sent, which was significantly more mature in tone for having waited 24 hours before writing it

My wife and I are both HBS '89 grads. We own and actively manage a small to medium size service business. I was encouraged at our last reunion to hear a lot of the effort HBS seems to be placing on small business and entrepreneurship.

However, I was horrified to see an HBS professor (prof Edelman) in the news harassing a small business over a small mistake on its web site. I don't typically get worked up about Harvard grads acting out, but in this particular case his actions are absolutely at the core of what is making the operation of a small business increasingly impossible in this country.

Small businesses face huge and growing compliance risks from almost every direction -- labor law, safety rules, environmental rules, consumer protection laws, bounty programs like California prop 65, etc. What all these have in common is that they impose huge penalties for tiny mistakes, mistakes that can be avoided only by the application of enormous numbers of labor hours in compliance activities. These compliance costs are relatively easy for large companies to bear, but back-breaking for small companies.

So it is infuriating to see an HBS professor attempting to impose yet another large cost on a small business for a tiny mistake, particularly when the proprietor's response was handled so well. Seriously, as an aside, I took service management from Ben Shapiro back in the day and I could easily see the restaurateur involved being featured positively in a case study. He does all the same things I learned at HBS -- reading every customer comment personally, responding personally to complaints, bending over backwards to offer more than needed in order to save the relationship with the customer.

As for the restaurateur's web site mistake -- even in a larger, multi-site company, I as owner do all my own web work. Just as I do a million other things to keep things running. And it is hard, in fact virtually impossible, to keep all of our web sites up to date. Which is why Professor Edelman's response just demonstrates to me that for all HBS talks about entrepreneurship, the faculty at HBS is still more attuned to large corporations and how they operate with their enormous staff resources rather than to small businesses.

Large corporations are crushing smaller ones in industry after industry because of the economy of scale they have in managing such compliance issues. If the HBS faculty were truly committed to entrepreneurship, it should be thinking about how technology and process can be harnessed by smaller businesses to reduce the relative costs of these activities. How, for example, can I keep up with 150+ locations that each need a web presence when my sales per site are so much less than that of a larger corporation? This is not impossible -- I have learned some tools and techniques over time -- and we should be teaching and expanding these, rather than spending time raising the cost of compliance for small business.

We are trying to use some of the available tools out there to better automate our application and onboarding process for employees. Though we are not a huge employer (about 350 part-time people) we hire and fire them all every year, so there is a lot of burden for our size on the HR system.

We are running into a frustrating issue. Most of our employees are older and often have limited computer skills, but we are getting past that. But we tend to hire couples, and it turns out in the over-50 set that couples often share the same email address. I can't even imagine having the same email address as my wife and having to filter through all of her business, but there it is. Unfortunately, in the world of web accounts, must vendors use the email address as the one reliable unique identifier for a person and thus use it for the user name or expect it to be unique.

This is throwing us for a loop. It is less of a problem in the application system because most of our couples just want to submit a single joint application anyway. But for onboarding, they each need their own W-4, I-9, etc. So they need separate user accounts.

The question then comes down to this for us: I can require them to get a second email address, but that is likely going to flummox some folks and require my manual intervention to help them. Do I thus cause more tech support issues for myself than I save from the automation itself?

No point here, just venting on a problem I have not figured out how to fix. And no fair saying stuff like "gmail is free and easy to sign up for, just make them get another gmail account." I have managers who do a fabulous job for me that it took me days to teach how to log into and use Gmail. A better and fairer comment would be "you have 20,000 applicants, make the application process require separate emails and even make it a little technically challenging so you limit your hiring pool to people who are better suited to using modern computer tools." And yes, that may in fact be our solution.

I think folks are rightly concerned that "disparate impact" logic run amok is leading to a lot of questionable practices, like this one in Minnesota:

The good: Minneapolis Public Schools want to decrease total suspensions for non-violent infractions of school rules.

The bad: The district has pledged to do this by implementing a special review system for cases where a black or Latino student is disciplined. Only minority students will enjoy this special privilege.

That seems purposefully unconstitutional—and is likely illegal, according to certain legal minds.

The new policy is the result of negotiations between MPS and the Department of Education's Office for Civil Rights. Minority students are disciplined at much higher rates than white students, and for two years the federal government has investigated whether that statistic was the result of institutional racism.

I understand the concern here, and I don't think it is unreasonable to demand that a public institution make this review process applicable to all suspensions, not just to those of black and Hispanic kids.

But good God, if I found out, say, that Hispanics were getting laid off at ten times the rate as Anglo workers in my company, I would definitely do something different in the process. I would not immediately assume it was due to discrimination but I would sure as hell insert myself into the process to make sure things were fair. I could easily see myself at least temporarily demanding in such a case that all terminations of people of color be reviewed with me first. Hell, I wouldn't have waited for two years to do it either. Even if the terminations turned out to be righteous, I would hopefully learn something along the way about why the disparity exists and what I could do about it in the future.

By the way, in today's legal environment, any private employer who says they don't put extra scrutiny on terminations of folks in protected classes, or don't increase the warnings and documentation required internally before firing someone in a protected class, is probably a liar.

This Starbucks story illustrates the hardest part about running a service business

"Pregnant woman denied Starbucks bathroom useage"